A colleague of mine (thanks Agnès!) informed me that the United Kingdom made public its data about startups. This is just amazing!

So I checked about Revolut and found all the data I could dream of. Founders, rounds of funding, shareholders.

Two young founders from Eastern Europe origin, 29 and 30-year old at the time of founding.

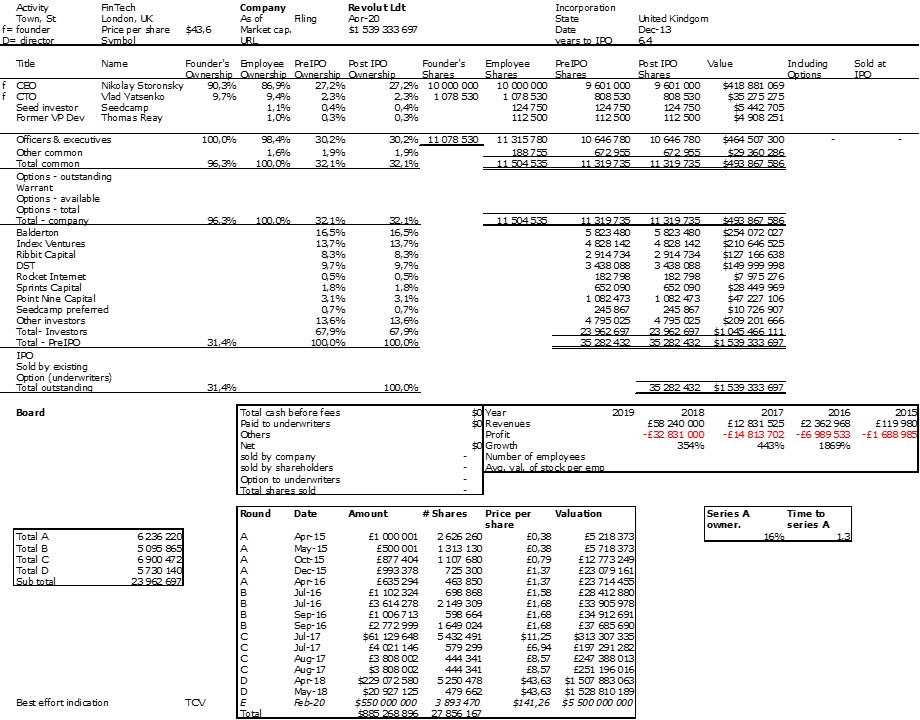

Some big, somewhat strange, rounds and here is today’s cap table. However series E is a best guest whereas previous rounds were publicly availale.

Comments welcome!

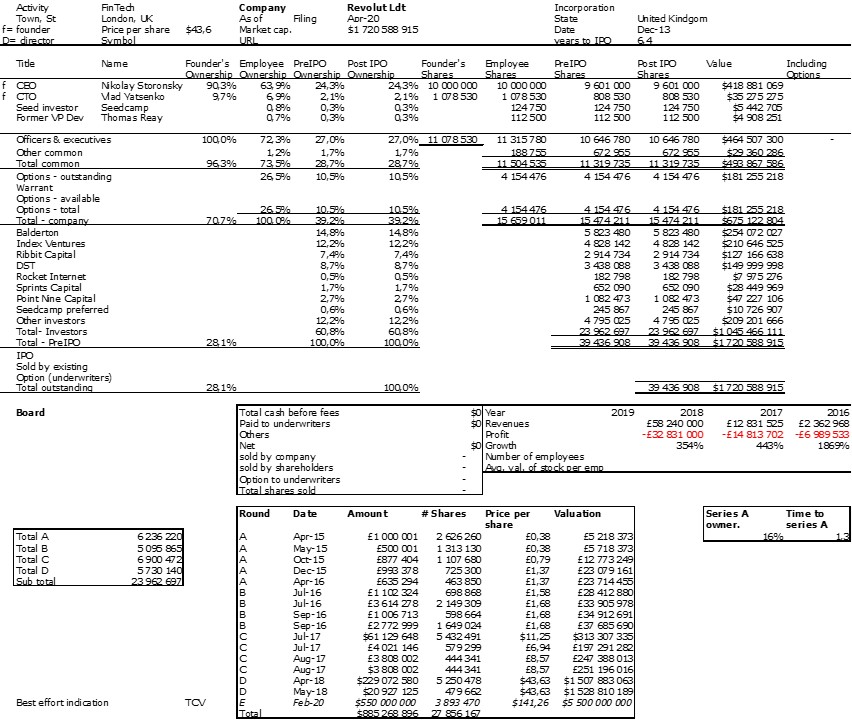

This morning (April 13), I discovered an important inaccuracy, nothing wrong but still: what about the ESOP, the stock-options. They are mentioned in the company documents, so here is a modified cap. table, and see the difference! I must add this is the ESOP in Dec. 2018, so the number is probably bigger today.

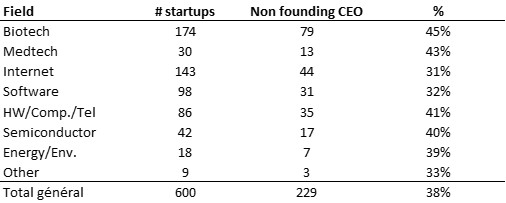

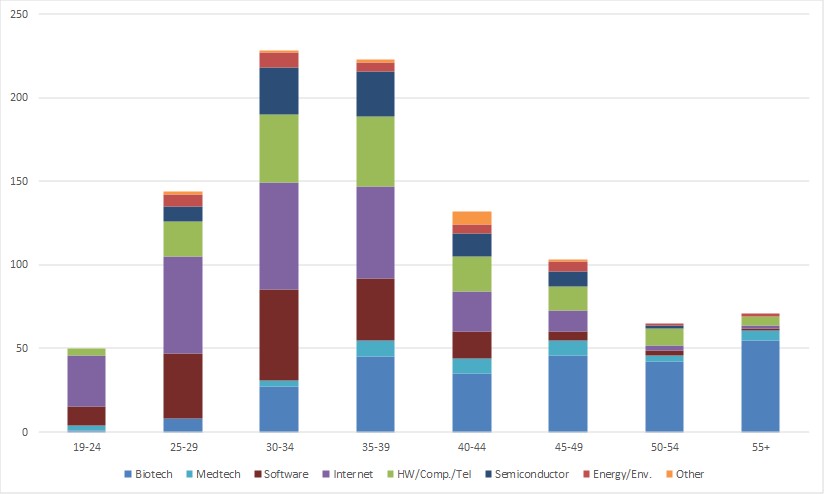

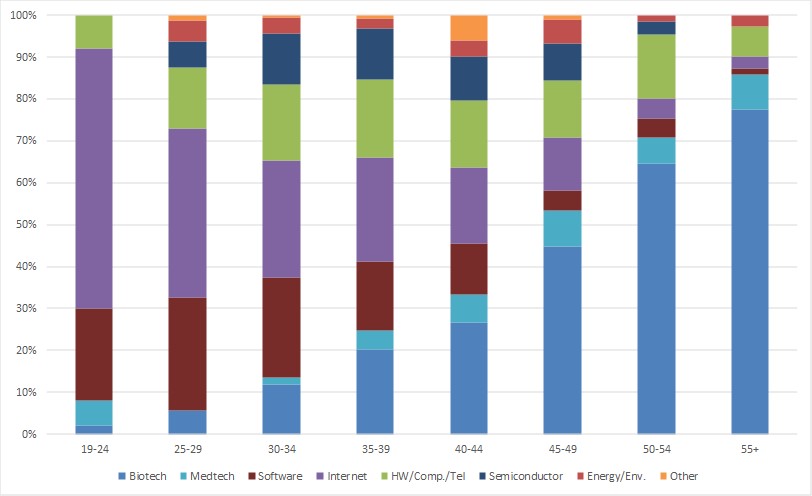

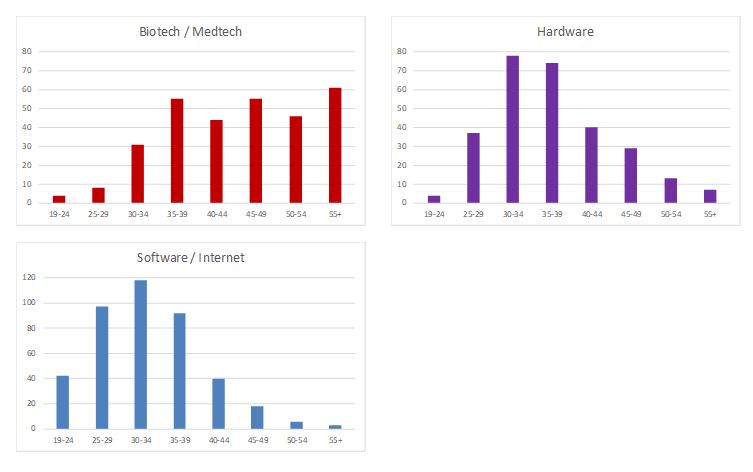

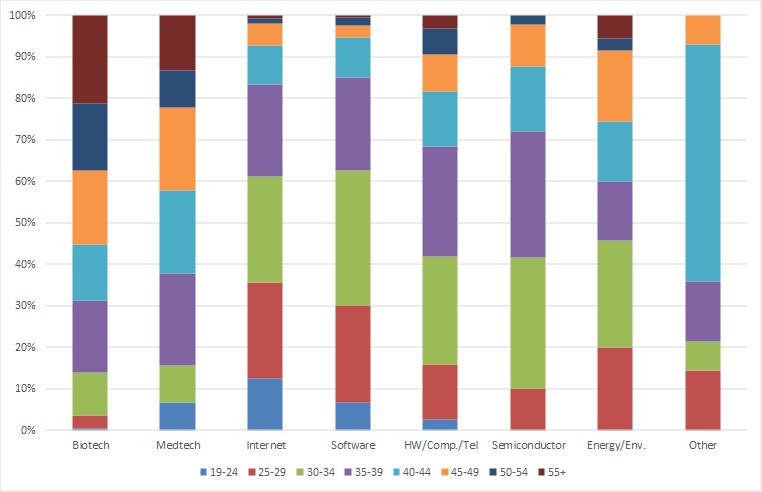

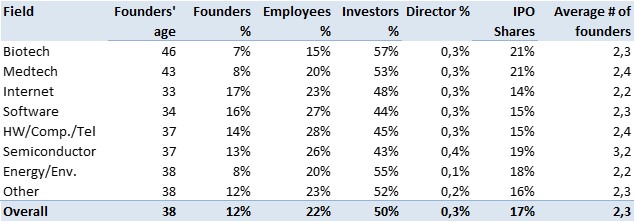

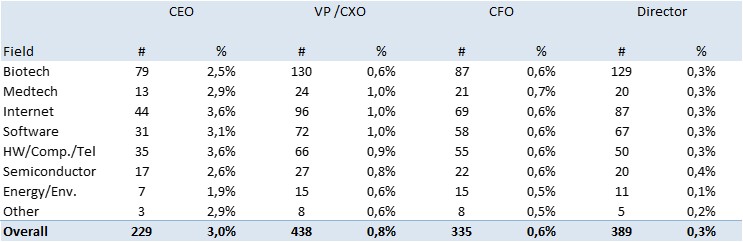

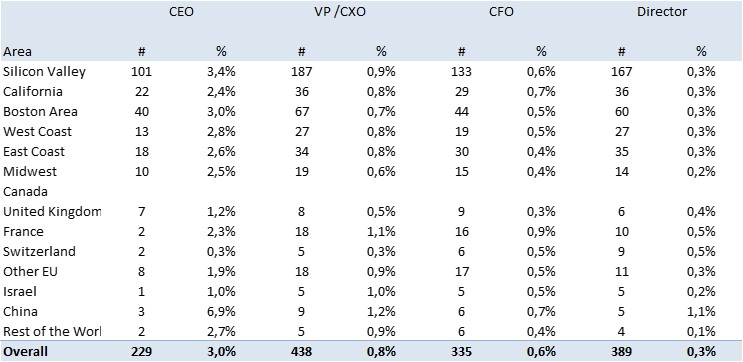

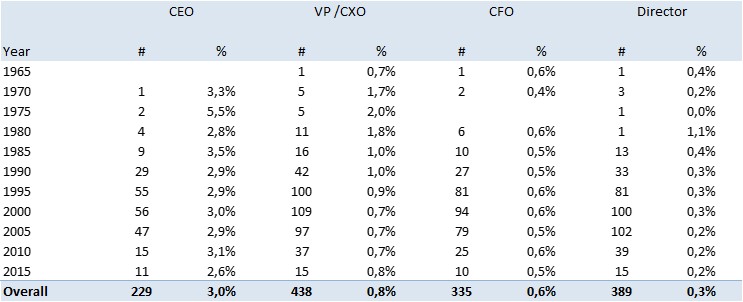

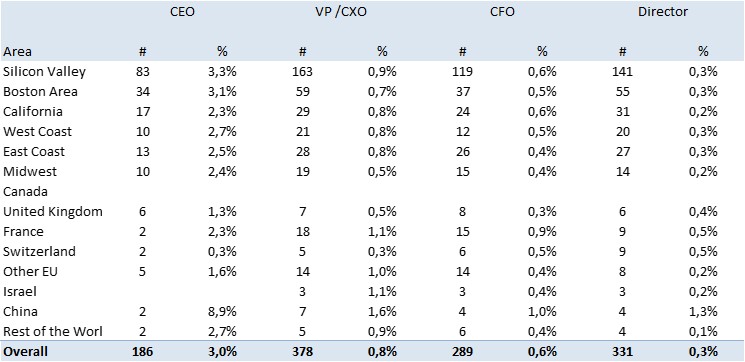

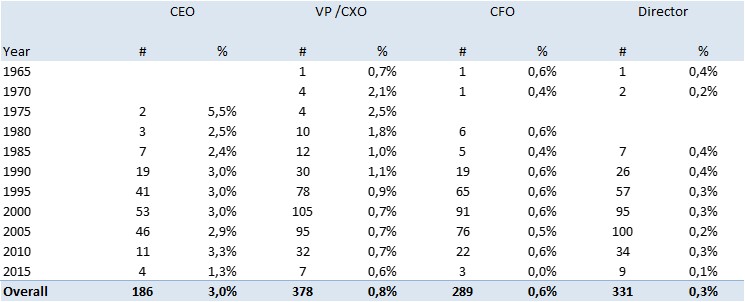

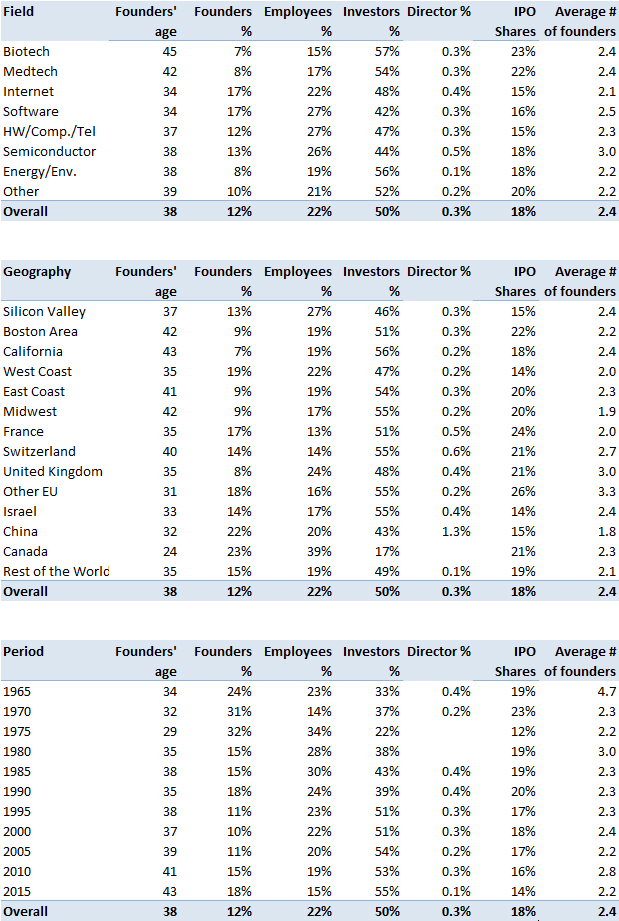

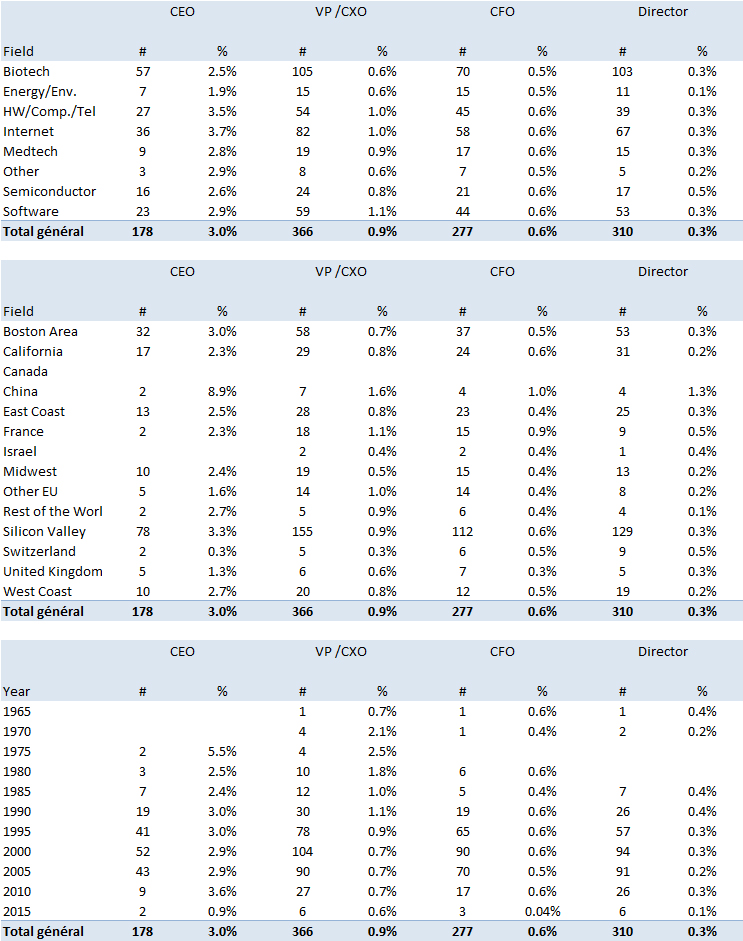

Fifth post of comments on the 600 startup data. Today, it’s about the ownership of non-founding CEOs (compared to the founders).

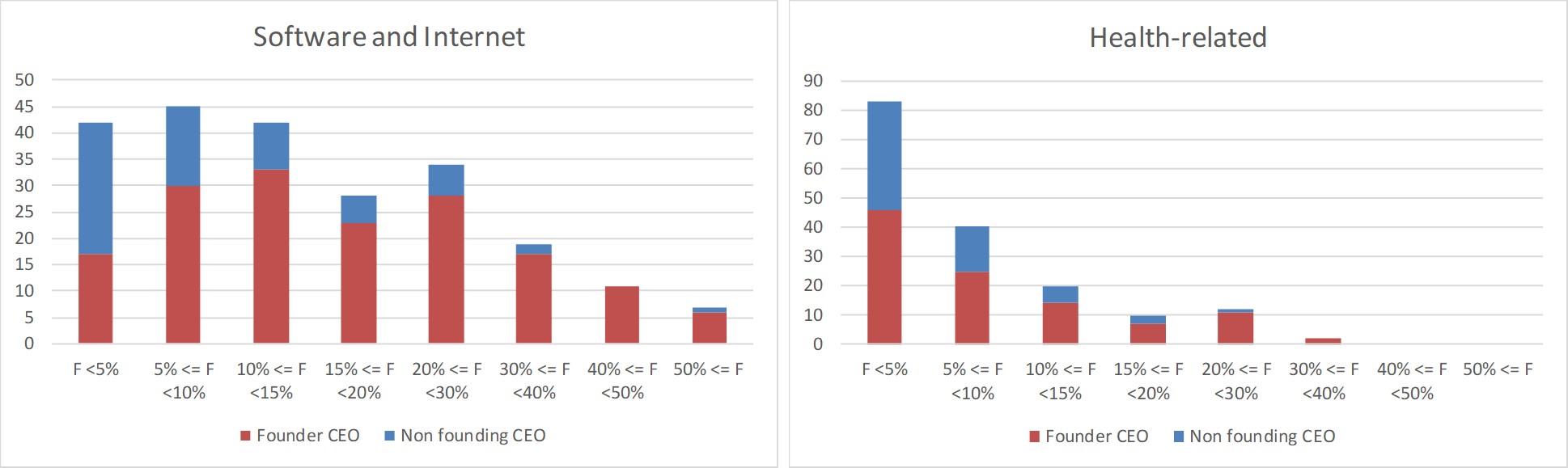

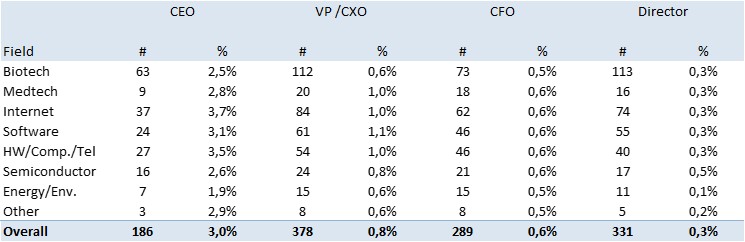

I noticed a few months ago that in a majority of cases, the CEO was a founder. This was a surprise. The data confirms this: there are a total of 229 startups with a non-founding CEO out of 600 (38%). Again, fewer in the digital domain, and more in the health-related fields.

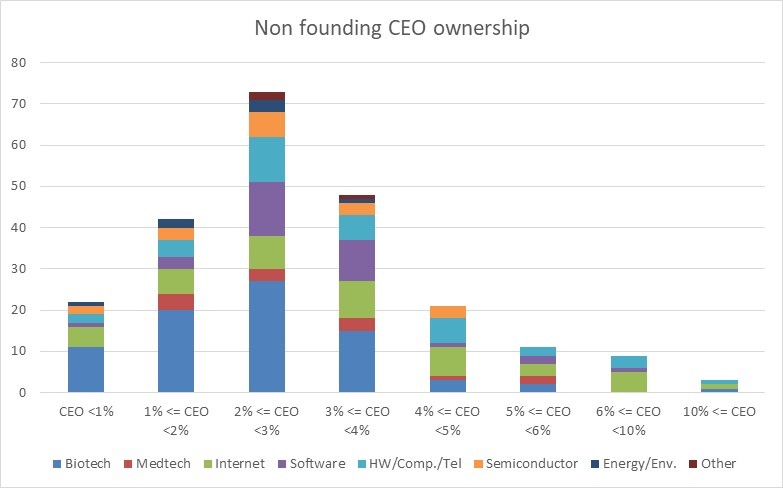

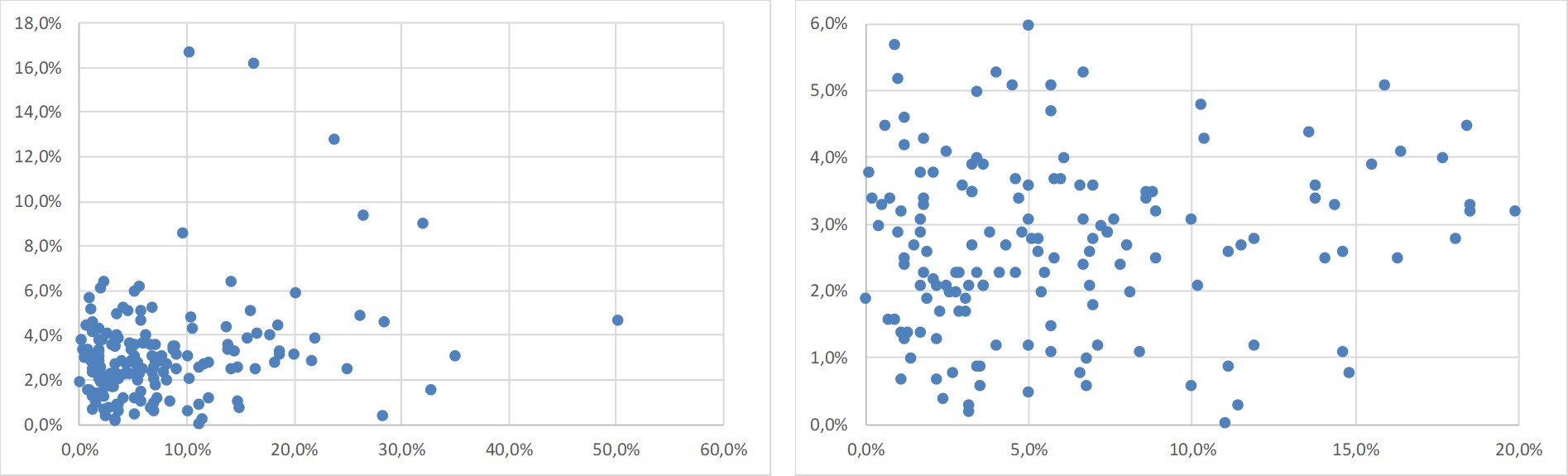

As you may see in my initial post, these CEOS have on average a 3% ownership (median value is 2.7%).

Is all this useful in practice? The median value of the ratio between the CEO & founders’s ownership is 0,5 (the average value is 1 because there are big outliers). Does this mean that if founders want to hire a CEO at foundation, he should have about 33% of the company, and at series A about 15% if you have read all my posts before!

Here is a more granular illustration.

The next image shows the founders’ ownership on the horizontal axis vs. the CEO’s on the vertical axis (with a zoom on the right).

A final illustration as food for thought, the founders’ ownership in the digital and health-related fields, relatively to the presence of a non-founding CEO or not. (Note that the vertical axis does not have the same scale for the two domains).

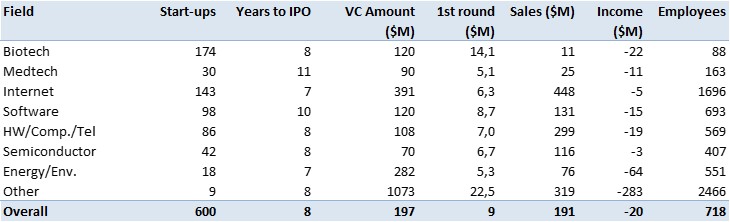

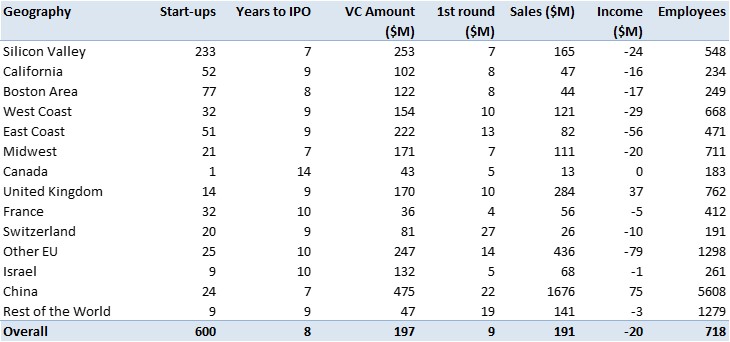

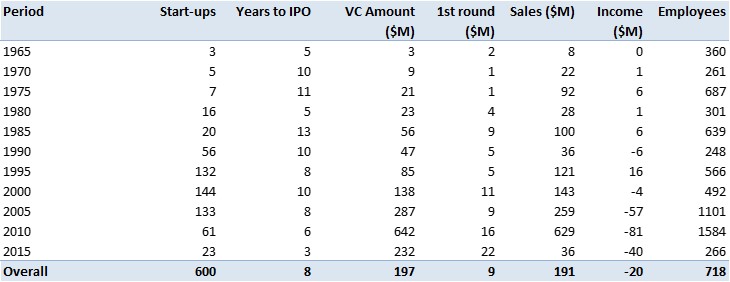

Third post of comments on the 600 startup data. As I am not sure how many posts I will write about this, I created a tag #600startups.

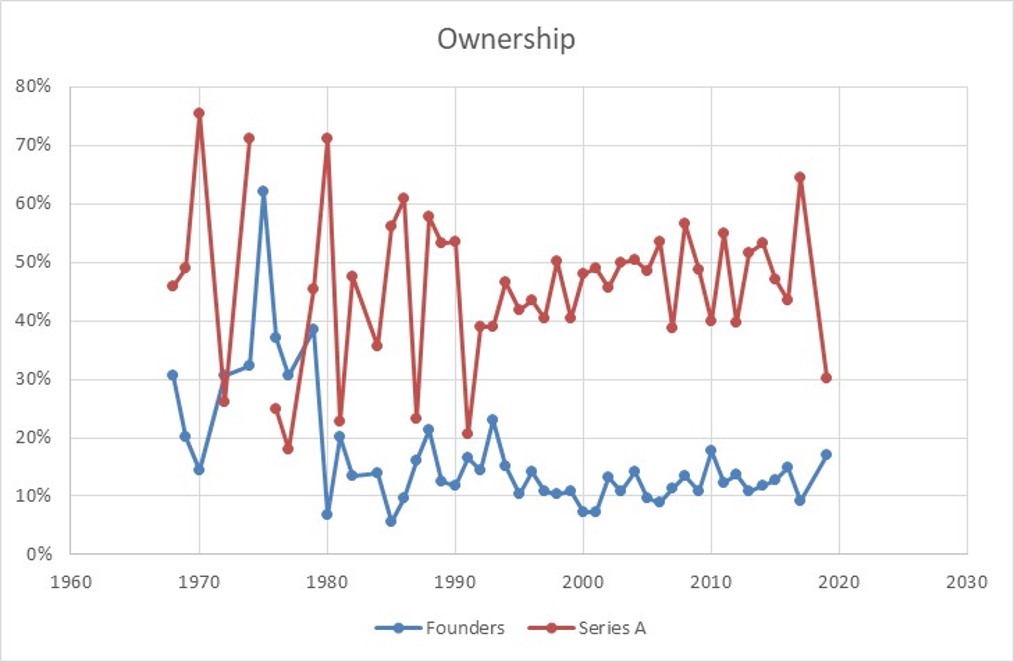

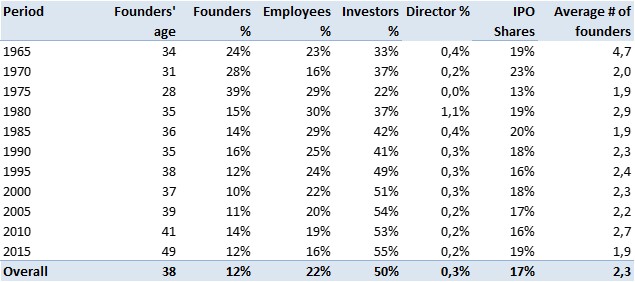

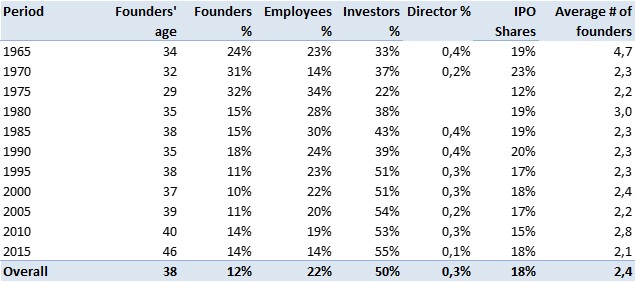

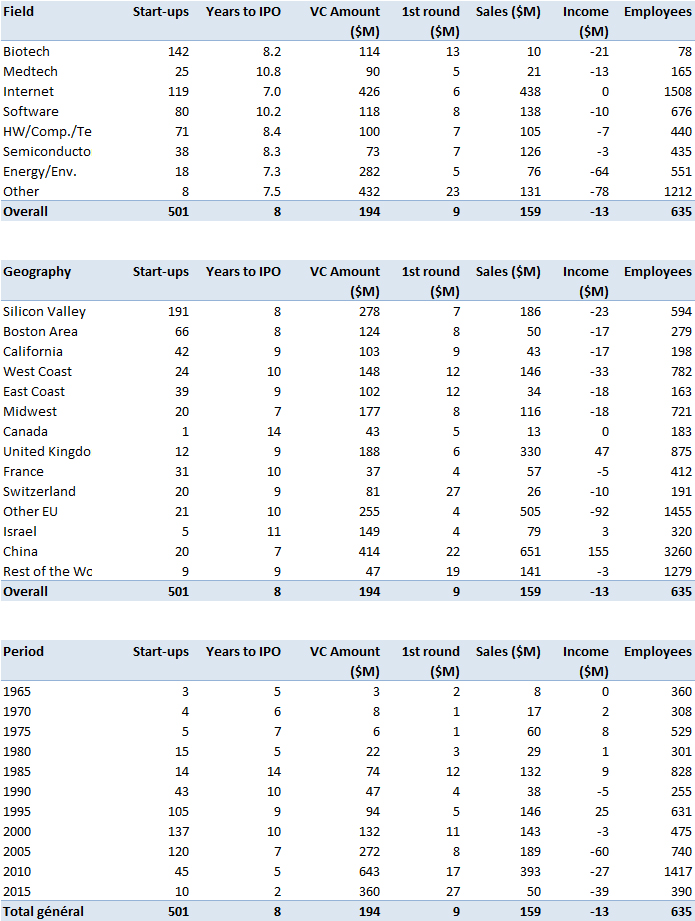

I looked at the founders’ age yesterday; today it is about their ownership over time. Founders keep 12.5% of the company at IPO, a little more in IT (about 16%), less in health (7-8%). The median value is 8.5%.

The series A curve is misleading! Founders’ ownership is at IPO but the Series A ownership is at the time of the round itself, not at the time of the IPO…

Moreover, I built a simple model which is the following: the Series A ownerhsip is based on the ratio between their shares and the sum of these shares and the founders shares increased by 20% (this to take into account future hires): as a short illustration, if Series A took 40% in the first round, founders had 50% as 10% was reserved for future hires (i. e. 20% of the founders’ stake).

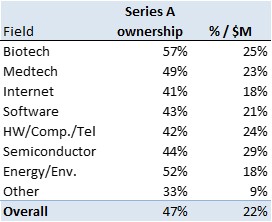

It’s also worth noticing the series A are pretty big, about $9M on average (median value is $4.5M), and possibly in several tranches (as it is quite common in biotech).

After venture capital in the first post, here are elements about founders.

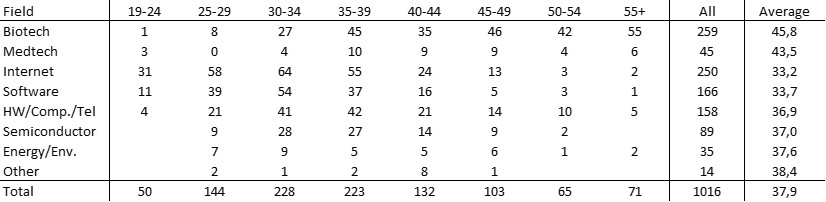

The 600 startups gave me data about 1016 founders, al though there is an average of 2.3 founders per startup. I did not have the age of all of them, neither their role or ownership. The average age is 37.9, the median is 36. (This is age at foundation, I added this after a comment I received on April 9, 2020).

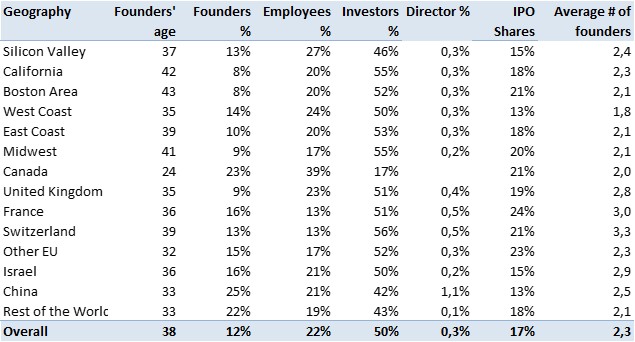

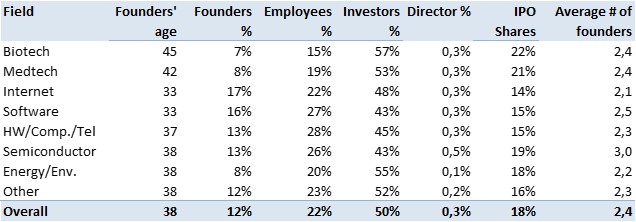

The following figures show some striking results about the age related to fields: founders are much older in the health-related fields, much younger in digital technnologies. It is more than 45 in biotech and 43 in medtech in comparison to 33 in software and Internet.

The Covid19 virus has an indirect effect, we have more time at home and in front of computers. So I updated my data in startup equity from 600 companies for which information was available, mostly because they had filed to go public. Here is the full list of individual data.

At the end of this 600+-page document, you’ll find some statistics, here they are again. I will probably come back to some results I find interesting not to say intriguing. Enjoy an react!

Some addtional comments in later posts:

1- About venture capital: on April 7 comments 1.

2- About the age of founders: on April 8 comments 2.

3- About the equity of founders: on April 9 comments 3.

4- How is equity shared: on April 10, comments 4.

5- About the equity of non-founding CEOS: on April 11, comments 5.

6- About valuation of startups: on April 12, comments 6.

7- What have they become: on April 16, comments 7.

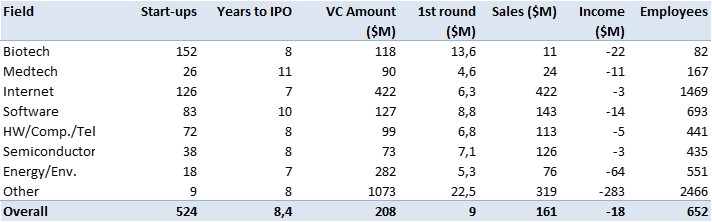

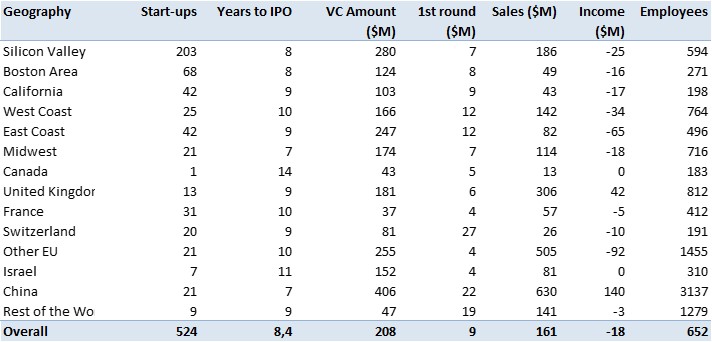

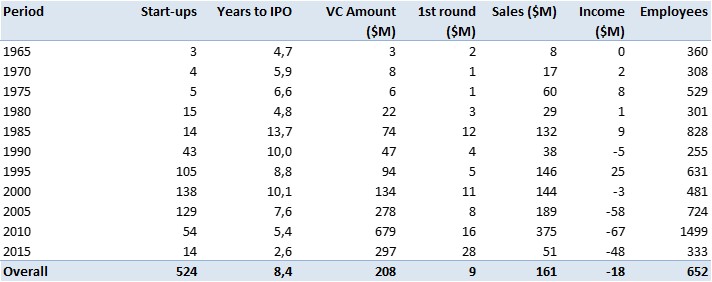

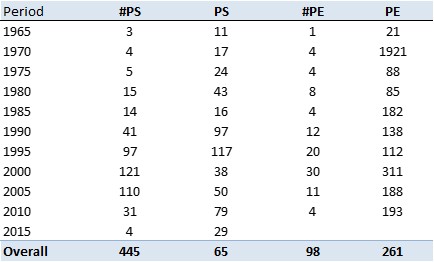

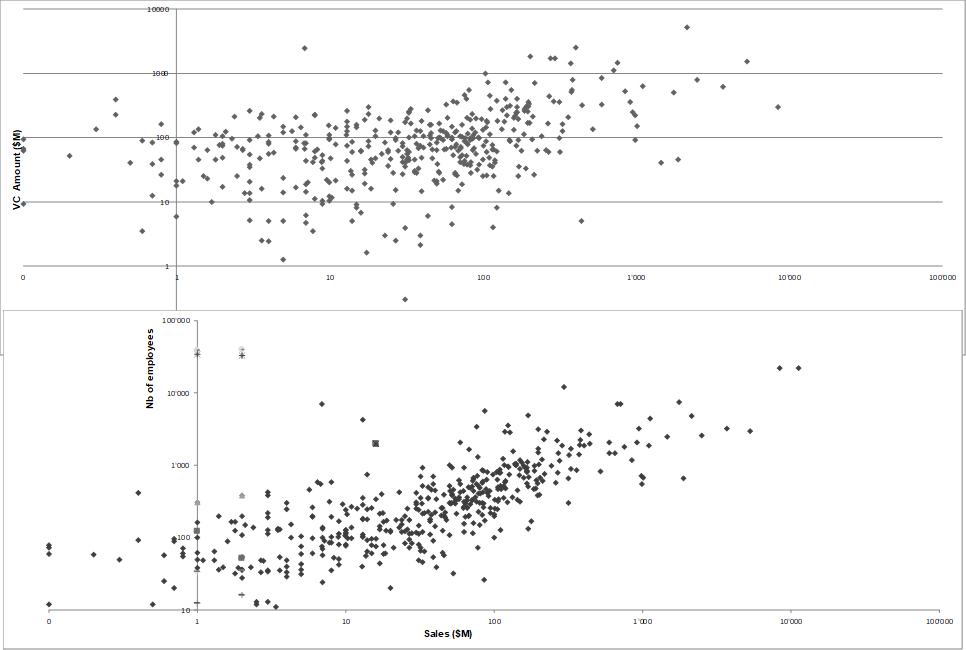

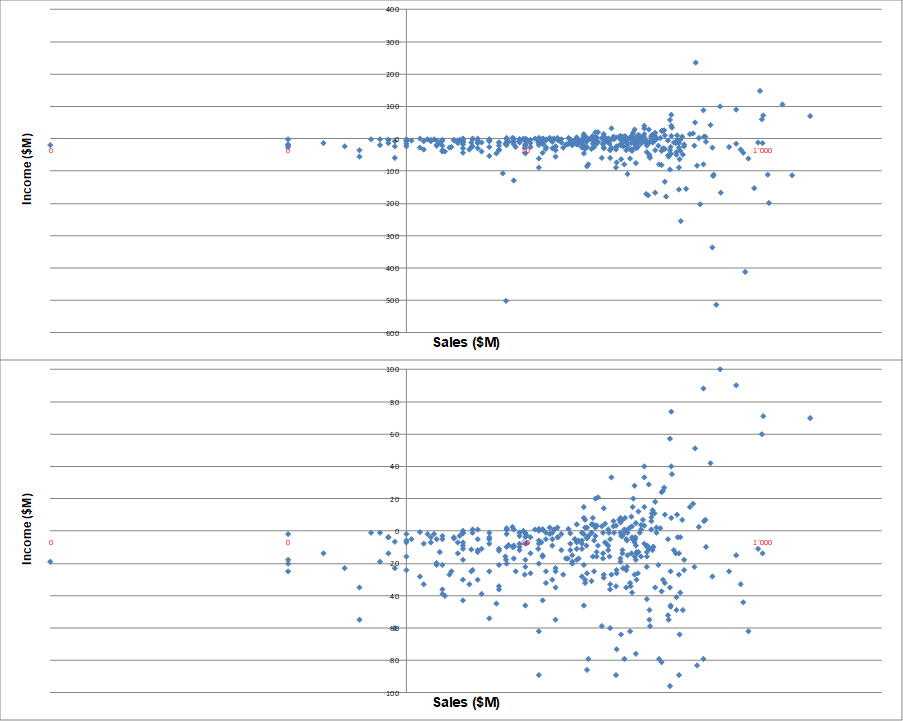

Basic data about startups (funding, sales, profits, employees at IPO and years to IPO) by fields, geographies and periods of time.

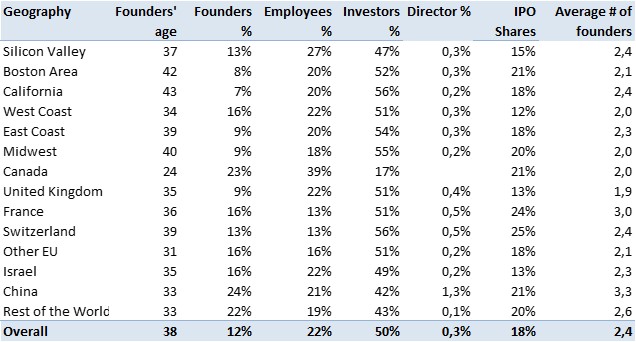

Data about founders (age, ownership and nb. by startups) and other stakeholders by fields, geographies and periods of time.

Data about ownership of non-founding CEOs, VPs, CXOs, board members by fields, geographies and periods of time.

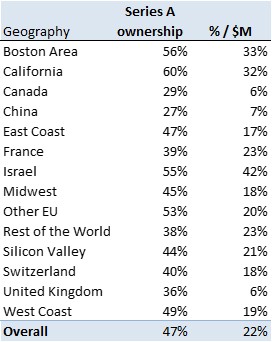

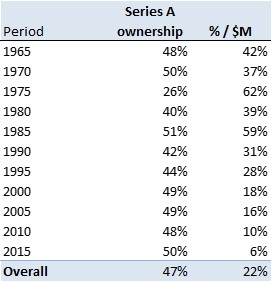

New data about ownership of series A investors by fields, geographies and periods of time.

Speculation, bubbles, yes, they have always been around. I entered the VC world in the late 90s. Now we are in the unicorns era. Or were we?

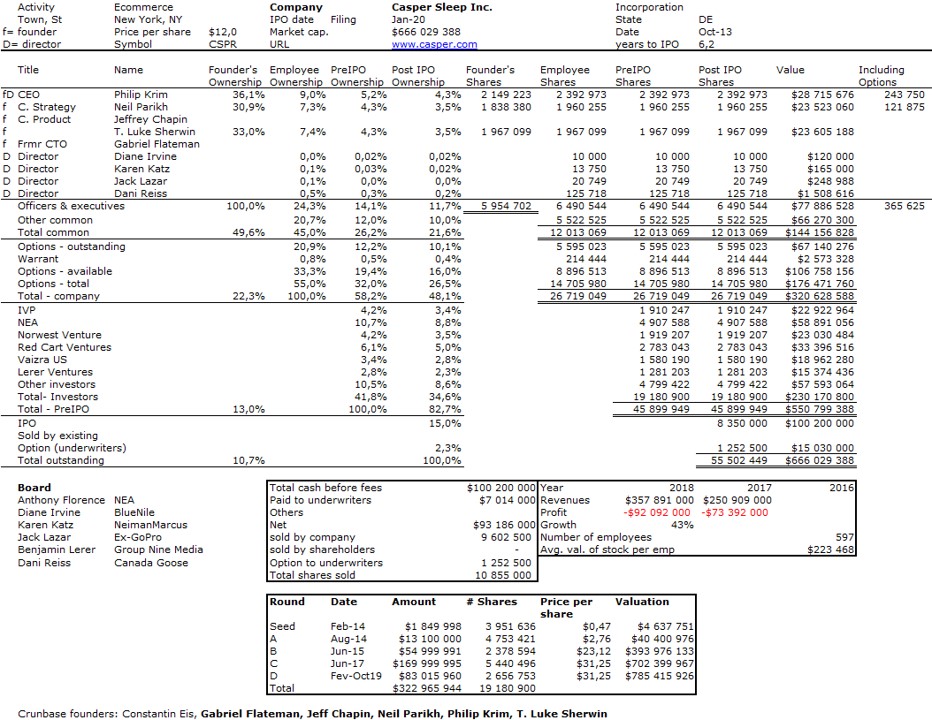

I did my 537th startup cap. table a few days ago (see below). I had hesitated a little as I was not sure a company selling mattresses, even online, could be classified in my list of tech companies. But with VCs like NEA, IVP, Norwest on board and leading banks such as Goldman Sachs and Morgan Stanley as underwriters, it had all the needed pedigree. Or at least it looked like it.

Then I read Casper’s IPO is officially a disaster on CNN and Here’s why Casper’s disappointing IPO could spell disaster for other unicorns on Business Insider Nordic

What happened? Well the initial IPO price on the table below should have been $18, then it was fixed at $12 for the first day of trading and this morning CSPR is at $10.26. The unicorn is now a $400M company. And you may want to have a look at the price of the B, C and D preferred rounds on the table below. Yes disasters happen from time to time.

As a quick remined my latest list to be updated when I will have reached 550 tables.

I had a few days ago a conversation about why I thought titles such as CEO or CTO were not such a good idea in start-ups. I thought this was a close debate and apparently not. So let me try to elaborate.

A good quote – I just found trying to structure my thinking – is “CEO means in a startup Chief Everything Officer”! CTO means someone who does not want to interact with customers while Business Development means the opposite. But you would not use VP of Sales in a small team…

In the book Startup Nation, there is something similar: “The multitasking mentality produces an environment in which job titles — and the compartmentalization that goes along with them — don’t mean much.”

Steve Blank explains titles are for established companies with knwon business models and known processes: Companies Have Titles to Execute a Known Business Model. […] Therefore the job title “Sales” in an existing company is all about execution around a series of “knowns.” [For example] Did he have a repeatable and scalable business model? Did he have a well understood group of customers? […] Startups Need Different Titles to Search For an Unknown Business Model. You didn’t need a VP of Sales, you needed something very different. Searching around a series of unknowns. You needed a VP of Customer Development

I am not sure I am allowed to do the following but here is a long extract from Bussgang: “Job titles make sense for mature companies, not for start-ups. […] At business school, I learned all about titles and hierarchies and the importance of organizational structure. When I joined my first start-up after graduation, e-commerce leader Open Market, I found the operating philosophy of the founder jarring: He declared no one would have titles in the first few years. If you needed a title for external reasons, our founder told us, we should feel free to make one up. But we would avoid using labels internally. In other words, there would be no “vice-president” or “director” or other such hierarchical denominations.

Why? Because a start-up is so fluid, roles changes, responsibilities evolve and reporting structures move around fluidly. Titles represent friction, pure and simple, and the one thing you want to reduce in a start-up is friction. By avoiding titles, you avoid early employees getting fixated on their role, who they report to, and what their scope of responsibility is – all things that rapidly change in a company’s first year or two.

So when I co-founded Upromise, I instituted a similar policy. We had an open office structure and functional teams, but a fluid organizational environment and rapid growth. One of our young team members changed jobs four times in her first year. Only after the first year, as we settled into a more stable organizational structure and I recruited senior executives who were more obviously going to serve as my direct reports on the executive team did I begin to give out titles (CTO, CMO, CFO, etc.). But you can establish role and process clarity without having to depend on titles.

Here is Steve Blank visual summary of all this:

In his four steps to the epiphany, he adds a quick check list about this: Goal of phase O-b: Set up the Customer Development Team. Agree on Customer Development team methodology and goals.

Author: Whoever is acting as CEO

Approval: Entire Founding Team/Board

Presenter: CEO

Time/Effort: 1/2-l day meeting of entire founding team

A- Review the organizational differences between Product and Customer Development – Traditional titles versus functional ones.

1. No VP of Sales

2. No VP of Marketing

3. No VP of Business Development

B-Identify the four key functional roles for the first four phases of a startup

1. Who is the Business Visionary

2. Who is the Business Execution

3. Who is the Technical Visionary

4. Who is the Technical Execution

C-Review the goals of each of the roles for each of the four Customer Development phases

D-Enumerate 3 to 5 Core Values of the Founding Team

1. Not a mission statement

2. Not about profit or products

3. Core ideology is about what the company believes in

Phase O-b Exit Criteria: Buy-in of the team and board for functional job descriptions, right people in those jobs, core values

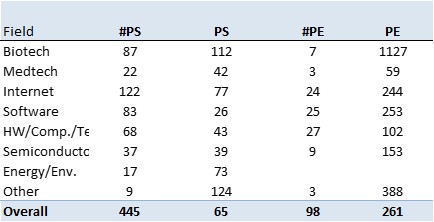

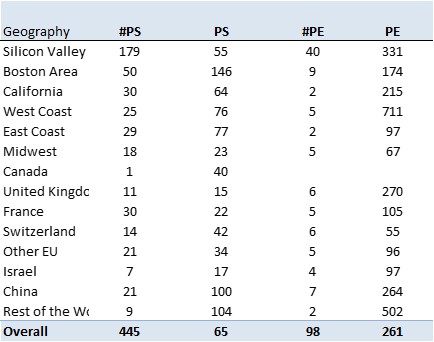

Here is an updated version of my equity tables from startups which filed to go public at some point. There are about 525 individual companies as well as just below statistical synthesis relatively to fields, geography and periods of time about VC amounts, time to IPO, levels of sales and income at IPO (as well as PS and PE ratios), age of founders, number of founders, ownership in companies by catagories. I think ths may be of interest for some of you…

Following my traditional analysis of startups through their IPO filings documents (you can check my 2017 analysis on 400+ documents here or the tag #equity on this blog), here is an updated analysis with 500+ start-ups.

You can have a look at the full 500 cap. tables on scribd or look at a shorter synthesis which follows.I hope this is self-explanatory enough.

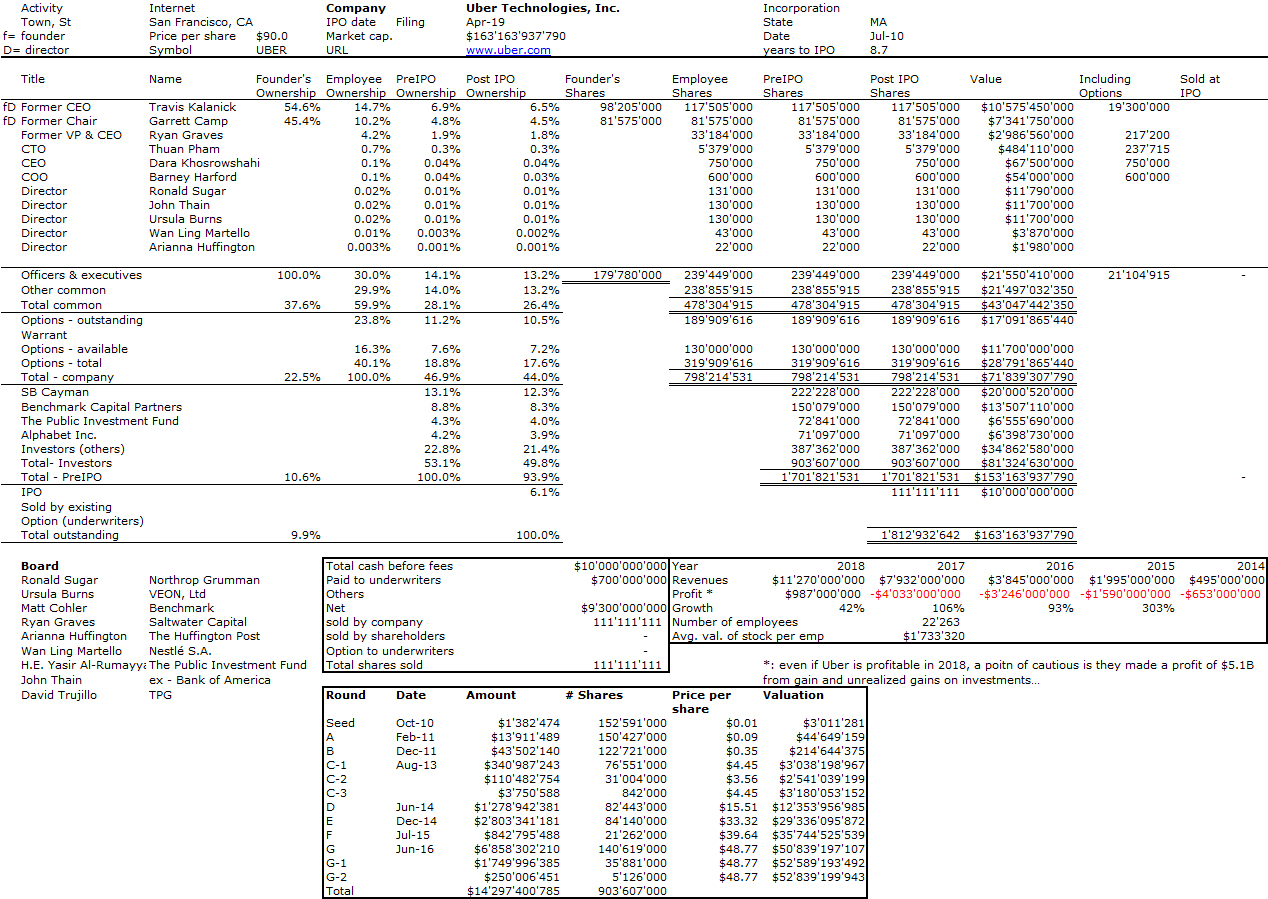

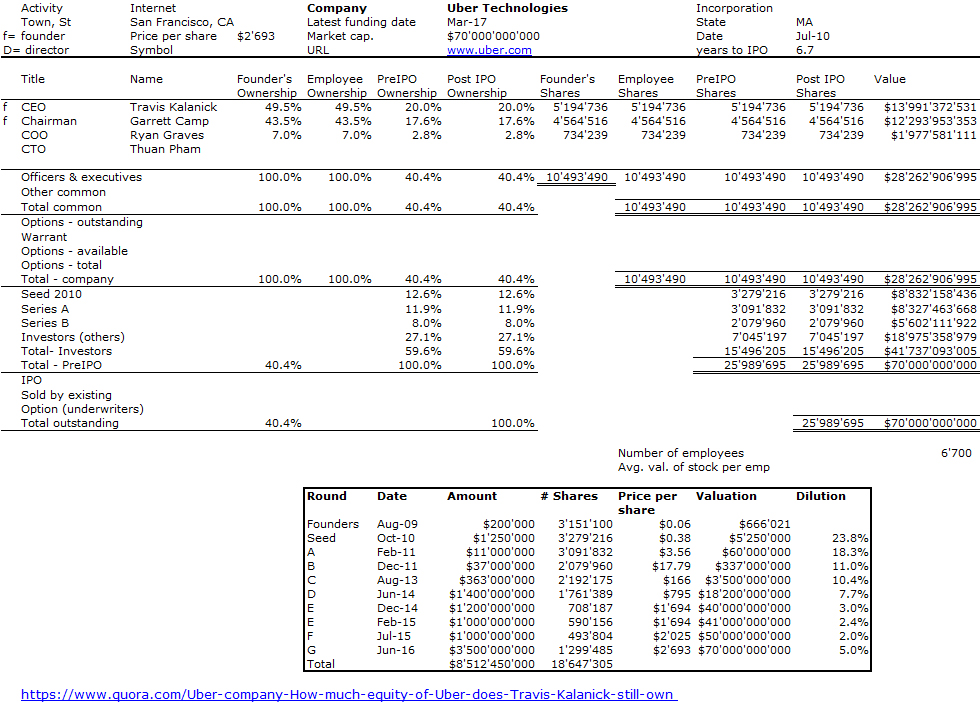

Uber’s S-1 has just been released. I jumped on the opportunity to analyze the shareholding of the startup, a thing I had tried to do in 2017 (with much less information – check here). Here are the figures that I found (subject to errors related to my possible too much eagerness…)

Uber cap. table – from the SEC S-1 published on April 12, 2019