Last October I published a post about the article The Case Against Patents by Michele Boldrin and David K. Levine. I had mentioned at the end that there was also a book, entitled Against Intellectual Monopoly. I am not finished with it yet but it is so strange, powerful and complex that I will talk about it in two parts. More in a few days…

It’s a very strange book (and the authors have been known for their arguments for a few years now) because it gives arguments against intellectual property (“IP”). They are not always easy to follow. This is a book about economics which sometimes, often (but not always) confirms the intuition that there is something wrong about IP. Yes inventors, innovators, creators need to be able to protect their creation against thieves. Does it mean they should be given a monopoly (patents) or a right to prevent copy of their work (copyright)? This is what the authors try to address. You can now read my comments but I strongly advise you to read the book and its complex and fascinating arguments, even if in the end, you disagree with them! As a provocative statement, they finish their 1st chapter with: “This leads us to our final conclusion: intellectual property is an unnecessary evil”. [Page 12]

One of their strongest arguments is the following: “It is often argued that, especially in the biotechnology and software industries, patents are a good thing for small firms. Without patents, it is argued, small firms would lack any bargaining power and could not even try to challenge the larger incumbents. This argument is fallacious for at least two reasons. First, it does not even consider the most obvious counterfactual: How many new firms would enter and innovate if patents did not exist, that is, if the dominant firms did not prevent entry by holding patents on pretty much everything that is reasonably doable? For one small firm finding an empty niche in the patent forest, how many have been kept out by the fact that everything they wanted to use or produce was already patented but not licensed? Second, people arguing that patents are good for small firms do not realize that, because of the patent system, most small firms in these sectors are forced to set themselves up as one-idea companies, aiming only at being purchased by the big incumbent. In other words, the presence of a patent thicket creates an incentive not to compete with the monopolist, but to simply find something valuable to feed it, via a new patent, at the highest possible price, and then get out of the way.” [Page 82]

The following is nearly as strong: “The incentive to share information is especially strong in the early stages of an industry, when innovation is fast and furious. In these early stages, capacity constraints are binding, so cost reductions of competitors do not lower industry price, as the latter is completely determined by the willingness of consumers to pay for a novel and scarce good. The innovator correctly figures that by sharing his innovation he loses nothing, but may benefit from one of his competitors leapfrogging his technology and lowering his own cost. The economic gains from lowering own cost or improving own product, when capacity constraints are binding, are so large that they easily dwarf the gains from monopoly pricing. It is only when an industry is mature, cost-reducing or quality improving innovations are harder to come around, and productive capacity is no longer a constraint on demand that monopoly profits become relevant. In a nutshell, this is why firms in young, creative, and dynamic industries seldom rely on patents and copyrights, while those belonging to stagnant, inefficient, and obsolete industries desperately lobby for all kinds of intellectual property protections.” [Page 153]

You can stop here! Or read additional extracts below. Or as I advised go to the book…

“The crucial fact, though, is that the following causal sequence never took place, either in the US or anywhere in the world. The legislative branch passed a bill saying “patent protection is extended to inventions carried out in the area X”, where X was a yet un-developed area of economic activity. A few months, years, or even decades after the bill was passed, inventions surged in area X, which quickly turned into a new, innovative and booming industry. In fact, patentability always came after the industry had already emerged and matured on its own terms. A somewhat stronger test, which we owe to a doubtful reader of our work, is the following: can anyone mention even one single case of a new industry emerging due to the protection of existing patent laws? We cannot, and the doubtful reader could not either. Strange coincidence, is it not?” [Page 51]

In Italy, pharmaceutical products and processes were not covered by patents until 1978; the same was true in Switzerland for processes until 1954, and for products until 1977. [Page 52]

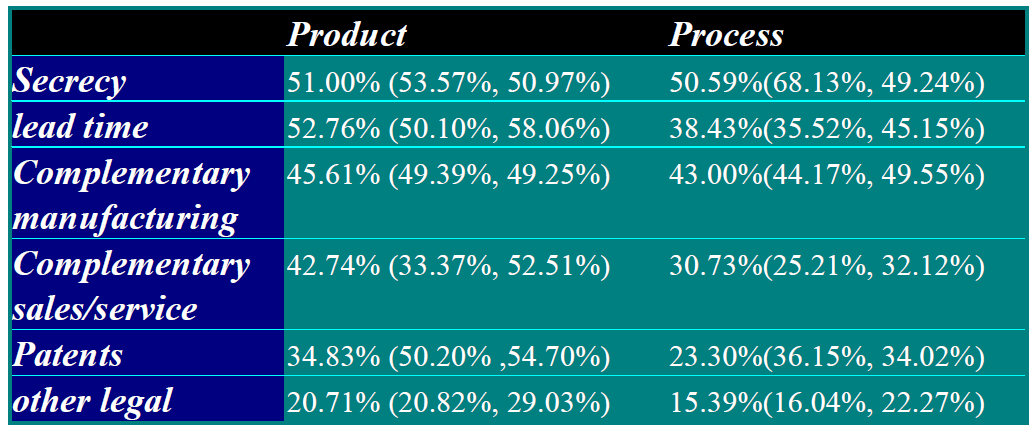

The firms were asked whether particular methods were effective in appropriating the gains from an innovation.The table below shows the percentage of firms indicating that the particular technique was effective. The numbers in parentheses are the corresponding figures for the pharmaceutical and medical equipment industries respectively: these are the two industries in which the highest percentage of respondents indicated that patents are effective. [Page 68]

“While patent pools eliminate the ill effects of patents within the pool – they leave the outsiders, well, outside.” [Page 70]

“Later in the book we talk about the Schumpeterian model of “dynamic efficiency” via “creative destruction.” The latter dreams of a continuous flow of innovation due to new entrants overtaking incumbents and becoming monopolists until new innovators quickly take their place. In this theory, new entrants work like mad to innovate, drawn by the enormous monopoly profits they will make. Our simple observation is that, by the same token, monopolists will also work like mad to retain their enormous monopoly profits. There is one small difference between incumbents and outsiders: the formers are bigger, richer, stronger and way better “connected.” David may have won once in the far past, but Goliath tends to win a lot more frequently these days. Hence, IP-inefficiency.” [Page 76]

“We understand that the careful reader will react to this argument by thinking “Well, the AIDS drugs may be cheap to produce now that they have been invented, but their invention did cost a substantial amount of money that drug companies should recover. If they do not sell at a high enough price, they will make losses, and stop doing research to fight AIDS.” This argument is correct, theoretically, but not so tight as a matter of fact. To avoid deviating from the main line of argument in this chapter we simply acknowledge the theoretical relevance of this counter-argument, and postpone a careful discussion until our penultimate chapter, which is about pharmaceutical research. For the time being, two caveats should suffice. The key word in the former statement is “enough”: how much profits amount to “enough profits?” The second caveat is a bit longer as it is concerned with price discrimination, and we examine it next.” [Page 77] There is a full chapter about Pharam, I will probably cover in part 2 of this article.

Jerry Baker, Senior Vice President of Oracle Corporation: “Our engineers and patent counsel have advised me that it may be virtually impossible to develop a complicated software product today without infringing numerous broad existing patents. … As a defensive strategy, Oracle has expended substantial money and effort to protect itself by selectively applying for patents which will present the best opportunities for cross-licensing between Oracle and other companies who may allege patent infringement. If such a claimant is also a software developer and marketer, we would hope to be able to use our pending patent applications to cross-license and leave our business unchanged.” [Page 80]

Roger Smith of IBM: “The IBM patent portfolio gains us the freedom to do what we need to do through cross-licensing—it gives us access to the inventions of others that are key to rapid innovation. Access is far more valuable to IBM than the fees it receives from its 9,000 active patents. There’s no direct calculation of this value, but it’s many times larger than the fee income, perhaps an order of magnitude larger.”[Page 84]

“Notice, in particular, that patenting is found to be a substitute for R&D, leading to a reduction of innovation. In the authors [Bessen and Hunt]’ calculation, innovative activity in the software industry would have been about 15% higher in the absence of patent protection for new software.” [Page 92]

An example of extreme aberration in U.S. Patent 6,025,810: “The present invention takes a transmission of energy, and instead of sending it through normal time and space, it pokes a small hole into another dimension, thus, sending the energy through a place which allows transmission of energy to exceed the speed of light.” [Page 101]

Arguments in favor of IP are known and quoted again by Levine and Boldrin… “In order to motivate research, successful innovators have to be compensated in some manner. The basic problem is that the creation of a new idea or design … is costly… It would be efficient ex post to make the existing discoveries freely available to all producers, but this practice fails to provide the ex ante incentives for further inventions. A tradeoff arises… between restrictions on the use of existing ideas and the rewards to inventive activity.”[Page 176]

A major element of the Beylat-Tambourin report (about which I have already published an article) addresses the concept of innovative ecosystems. Before mentioning some passages, here are two interesting references on this concept:

– Josh Lerner in his book Boulevard of Broken Dreams shows how entrepreneurs and investors have benefited from each other in situations of tension and collaborations in the 60-70s. He also shows the importance of public support at least in the early years (funding for the Cold War and support to venture capital – SBIR, Erisa) so that it can be said that “the public sector played a key role in the evolution of Silicon Valley”. Then he tries to show some errors: incompetence in the allocation of public resources, inefficient use of subsidies, by “organizations whose mandate is to help entrepreneurs” (“Seven incubators provided under 50% of funds for companies”- an example in Australia) and the SBIR program has reached its limits. Also, his recommendations are:

– enhancing the entrepreneurial culture [through the right laws, the access to technologies, tax incentives and training],

– increasing the start-ups attractiveness [through allowing partnerships, creating local markets, accessing human capital abroad],

– avoiding common mistakes: timing [be patient], sizing [not too small, not too large], flexibility [learn by doing], create the right incentives [and here it is a complex situation as perverse effects from good ideas often occur] and evaluate [which does not happen often enough]. Already in his introduction he writes that you need rules, experience, time, incentives and assessment. But with all his experience and knowledge about high-tech entrepreneurship, Lerner is very humble with the lessons: the topic is really complicated, all these advice have to be implemented together and it is really their careful interconnections which will make an ecosystem lively or not. There must obviously be a lot of talent.

– Brad Feld gives the ingredients of start-up ecosystems:

1. A Strong Pool of Tech Founders

2. Local Capital

3. Killer Events

4. Access to Great Universities

5. Motivated “Champions”

6. Local Press / Websites / Organizational Tools

7. Alumni Outreach

8. Wins

9. Recycled Capital

10. Second-Time Entrepreneurs

11. Ability To Attract a Pool of Engineers

12. Tent-pole Local Tech Companies

Back to Beylat Tambourin report : “Everywhere in the world, innovation is stimulated within networks of actors uniting training, research, young & fast growing companies (start-ups), service companies, large groups engaged in a policy of “open innovation”, professional coaching and innovation funding, and sometimes the hospital.”

The most emblematic examples are of course Silicon Valley, the Boston area or Israel. […] In Europe, most states began a decade ago to implement a policy of clusters: poles of competence in France (in addition to existing clusters), with a focus on collaborative R&D; more recently a focus on a small number of world-class Spitzencluster in Germany, etc.. The effectiveness of these networks is based on the fluidity and speed of “assets” of innovation skills (persons), technology, infrastructure, services and financing. Innovation is primarily a matter of stimulation and confrontation of different points of view. The role of clusters and innovative ecosystems, in this aspect of their business and not as factories of R&D projects, is critical.

The success of clusters at international level is now relatively well analyzed and relies heavily on a few factors:

– World-class universities

– An industry of venture capital aggregating institutional and private investors,

– A range of sophisticated services (HR, legal, marketing) to support the growth of young innovative enterprises,

– Professionals of high techonology

– A critical but intangible ingredient: an entrepreneurial culture.

Transfer processes and innovation are “naturally” complex for several reasons:

– The transfer takes place at the interface of two worlds with different logics, which requires to achieve and maintain a significant level of trade, trust, understanding of the issues and objectives of each other…

– Innovation can not be deployed within an “established” entity: this statement is largely based on the concept of open innovation (open innovation).

– The complexity of the transfer process and innovation also increases with the depth of research and the nature of disruptive innovation.

– The processes involved are not “deterministic”: set goals and define interim milestones is of course necessary to construct a “nominal” trajectory, but we must accept that the “real” path will be different, and it is better to be able to adapt than trying to predict the future.

-> The policy must finely understand the ecosystem dynamics: centralized methods are not effective, we must have a Darwinian system and continually assess.

The challenges of ecosystems

– The impossibility of identifying a “construction plan” of an ecosystem, from scratch or from some already present features: an ecosystem is built over time and then one notices it. The time required for its construction (often several decades!) just proves that any search for the “first cause” behind the ecosystem is futile. This is a hard point for governments who want to create an innovation ecosystem for a particular “field” on this or that “territory”. Local governments, national and European are generally funders but they must have the patience of investors.

– The complexity of measuring the effectiveness of an ecosystem: assessment is central, but difficult to implement. The evaluation of each of the players in the ecosystem is of course possible, if indeed they have clearly defined tasks and ways to fill them. However, all of these individual assessments is not an assessment of the ecosystem, according to Pascal’s principle that it is “impossible to know the parts without knowing the whole, nor to know the whole without knowing the parts”.

– An effective ecosystem is based on the acceptance of their role by each of the actors: all are necessary for the operation, but none can claim to be the sole cause of success. However, the temptation to declare oneself essential is much stronger as most actors depend on government subsidies and can consider themselves in competition for access to these resources. Each player must avoid both “sufficient and insufficient” and remember that one’s effectiveness depends largely on that of the ecosystem (or ecosystems) to which one belongs.

– “Simplify” or “optimize”an ecosystem, let alone a complex of ecosystems,is irrelevant: we must accept “Darwinism”, think articulations, and continuously assess the dynamics to maintain and improve the efficiency of public investment. Proposals for simplification and optimization from some players and / or public authorities (local, national, European) actually consist of creating a new “object” that is supposed to respond to the noted deficiencies : it is the illusion of the “exceptional measure” that will change the situation of innovation, the creation of a device or structure, which explains to a large extent the accumulation of devices and structures in France. The challenge, however, is to define the positioning of any new “object” within the existing structure (for an ecosystem is built over time) and explain how it will improve the efficiency of the overall system.

I had the pleasure to be part of the group who contributed to the Beylat-Tambourin report, Innovation: High Stakes for France, which subtitle is also important: Dynamizing the Growth of Innovative Companies. It was a long process, we started working in September and the final document was presented to the Ministers on 5 April. You can download the report in pdf format or here, should the previous one not work..

The report is in French but as I saw the Wall Street journal mentioning it, I thought I would do a post in English too. However, if you read French, go to the sister blog post: L’innovation en France: le rapport Beylat Tambourin. My French is much better!

What should be noted before discussing the content is that 25 members of the mission come from different worlds (see end of article), which could have made it difficult to find agreement. This was not the case. There were debates, but this report summarizes the proposals without forgetting important points, or dilute the point, I think. I read (only) one satirical article in the media, but I’m not sure that the author had read the report (see end of the article as well)…

Click on the image to download the report in pdf format

I translate (again my apologies for my far from perfect English) here a quote from the introduction: “With the acceleration and the complexity of the issues, public policies sometimes seem poor, often messy. […] They have often been compared to a system of research transfer, itself too weak, and indeed not focusing enough on the creation of high-growth companies with an ability to create jobs. […] But there is no single model of innovation. […] However, invariants exist: research excellence; low barriers between public and private sectors; an entrepreneurial culture; cultural diversity, the ability to attract talent at an international level; a migration policy; and a successful combination of start-ups, large corporations, public research, higher education and investors.” [Pages 1-2]

The difficult definition of innovation

Here’s a great paragraph that I want to quote again: “There is no definition – uncontested and incontestable-of innovation but it is possible to bring out some characteristics of innovation:

– Innovation is a long, unpredictable and hard to control process.

– Innovation is not limited to the invention and innovation is not only technological.

– At the end of this process, are created products, services or new processes that demonstrate that they meet the needs (market or non-market) and create value for all stakeholders.

Another point worth noting: an innovation cannot be decreed, cannot be planned, but it is seen through the commercial (or societal) success it meets. This explains why it often comes at the margins of existing businesses and through interactions with many different actors: “The Internet is the product of a unique combination of military strategy, scientific cooperation and protest innovation” in the famous sentence by Manuel Castells.” [Page 5] ” Accordingly, a vision where the expenditure on R&D is the main concern should be changed in favor of a systemic vision for results, in terms of growth and competitiveness.” [Page 6] In other words, innovation is not the invention and certainly not R&D.

Here are the 19 recommendations, divided into four groups:

I. Developing a culture of innovation and entrepreneurship.

II. Increase the economic impact of public research by the transfer.

III. Support the growth of innovative companies.

IV. Develop instruments of public policy for innovation.

For the first group (Culture):

1. Revise teaching methods in primary and secondary schools to develop innovative initiatives.

2. Implement a large-scale program for entrepreneurship learning in higher education.

3. Promote the dissemination from large groups through spin-offs.

4. Develop a policy for attractiveness of talent around innovation. For the second group (transfer):

5. Implement the operational monitoring of 15 measures for rebuilding the transfer of public research (see http://www.enseignementsup-recherche.gouv.fr/cid66110/une-nouvelle-politique-de-transfert-pour-la-recherche.html – in French)

6. Promote the mobility of researchers between the public and private sectors.

7. Develop a coherent program for the transfer through the creation of businesses.

8. Focus SATT on maturation [SATT are the new French structures for academic technology transfer].

9. Establish a consistent policy of public-private research partnerships, bringing together different policies (scattered today). For the third group (growth):

10. Address the lack of equity financing for innovative companies (venture capital and later-stage growth equity) by mobilizing a small part of the French savings and improving the possible exit strategies for investors in these segments.

11. Launch “early stage” sector initiatives.

12. Implement the policy instruments of protection (IP, standardization) serving innovative companies.

13. Harmonize the different labels of innovative companies for better readability and link them to the growth of companies, consistently aligning all support tools available.

14. Encourage large groups and large public institutions to be involved in the emergence and growth of innovative enterprises, integrating new dimensions in their obligation for environmental and social responsibility. Finally for the last group (public policy):

15. Recognize the role of metropolitan innovation ecosystems as the support for regional strategies as well as for the national innovation strategy.

16. Organize the transfer system to make it more readable and more efficient.

17. Provide the means to develop, pilot and evaluate a comprehensive and coherent strategy of French innovation.

18. Appoint a single operator for the operational consolidation of public finance policies of innovation: the BPI (the Investment Public Bank in its innovation component).

19. Making innovation a real political issue, organizing a broad public debate.

[Again sorry for the imperfect translation. I hope you got the points…]

As explained in the Wall Street Journal in Nineteen Ways to Make France More Innovative, “In the short-term, the government should move away from considering R&D spend as a metric of innovation recommended the authors, and look at jobs created. France outspent Germany on R&D in many areas, said Mr. Beylat and Mr. Tambourin, but the effect wasn’t felt in the economy.”

Another comment concerns the sub-title of the report: Dynamizing the Growth of Innovative Companies. This is a very important subtitle, but do not get me wrong, it is not about start-ups only here, but the message is that innovative companies should be a source of growth, whether large groups, SMEs or start-ups. It may not be a cultural revolution, or is it?

To push the envelope a little further, here is a short excerpt: “France is between the American dream of Silicon Valley, where disruptive innovations are supported by start-ups, the German dream of a well-established industrial Mittelstand, efficient in incremental innovation, and a French tradition of industrial planning in sovereign sectors. This oscillation blurs the representation that France has made of innovation because it mixes breakthrough innovation, incremental innovation and “strategic industrial policy.” We must cut short a myth: if innovation often requires an excellent R&D, it is not limited to R&D. It is not its natural extension. Innovation is above all the process that leads to the marketing of products or services, meeting a need, made by individuals engaged in an entrepreneurial approach. Innovation is thus at the crossroads of several areas, first and foremost research, entrepreneurship, industry and education. There is therefore no conceptual optimization or normative expected pattern.” [Page 6]

And on the cultural aspects: “Innovation is primarily a matter of individuals, state of mind and ambition for the company and for themselves. The dissemination of the culture of innovation and entrepreneurship is vital. These cultures are closely linked: vision, risk-taking, acceptance and learning from failure, capacity for initiative, project culture and commitment to completion are the main components. Finally, the ability to create companies with high growth potential (spin-offs and start-ups), some of which will become world leaders, sometimes in a few years, characterizes an effective innovation system.” [Page 7]

And finally I add a quote from President Obama, which perfectly symbolizes the problem: “We insist on personal responsibility and we celebrate individual initiative. We’re not entitled to success. We have to earn it. We honor the strivers, the dreamers, the risk-takers, the entrepreneurs who have always-been the driving forces behind our free enterprise system – the greatest engine of growth and prosperity the world has ever known.”

The report was presented to ministers on April 5, and to the French Prime Minister on April 8, for the appointment of Anne Lauvergeon as President of Innovation 2030. Genevieve Fioraso [the French minister for research and higher education] noted, however, in her introduction to the submission of this report, that President Obama was able to speak for about an hour on this one chapter of innovation. Where else would this be possible?

Finally, and this is a personal note, this report should be used more as a base for innovation than as a toolbox or a set of recipes. This is the big picture that matters and not the extraction of recommendations that would suit one or the other. “The issues of competitiveness show that innovation must be at the heart of public policy, as illustrated by our recommendations. While this is a technical issue that is inherently complex (because of all the dimensions that make up), where the “right” decisions are sometimes against-intuitive (eg, linear view of innovation seductive but wrong), it seems essential that innovation becomes a real political issue to ensure its adoption by policy makers and citizens.” [Page 121]

Finally I would like to add more quotes on innovative ecosystems. As it begins to be long, I’ll do it in a future article …

Facts and Figures

They show the challenges of innovation, particularly in France. I’ll let you judge for yourself.

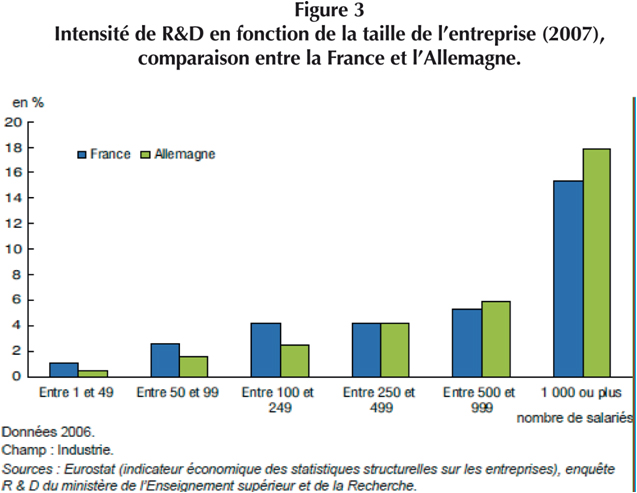

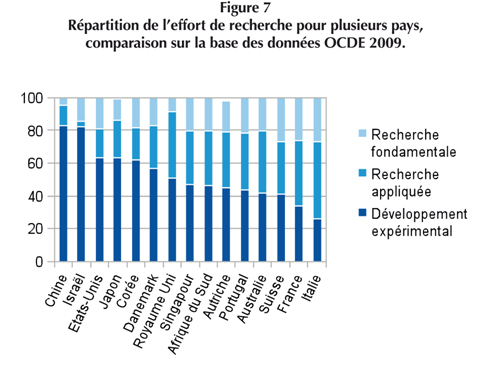

R&D Intensity (compares France and Germany in their R&D efforts relatively to firm size)

An interesting typology of research using fundamental and applied research as well as experimental development

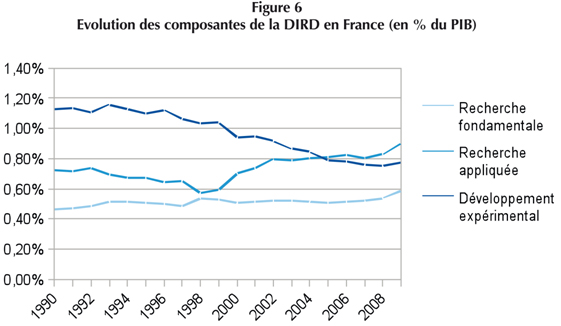

… and its evolution in France

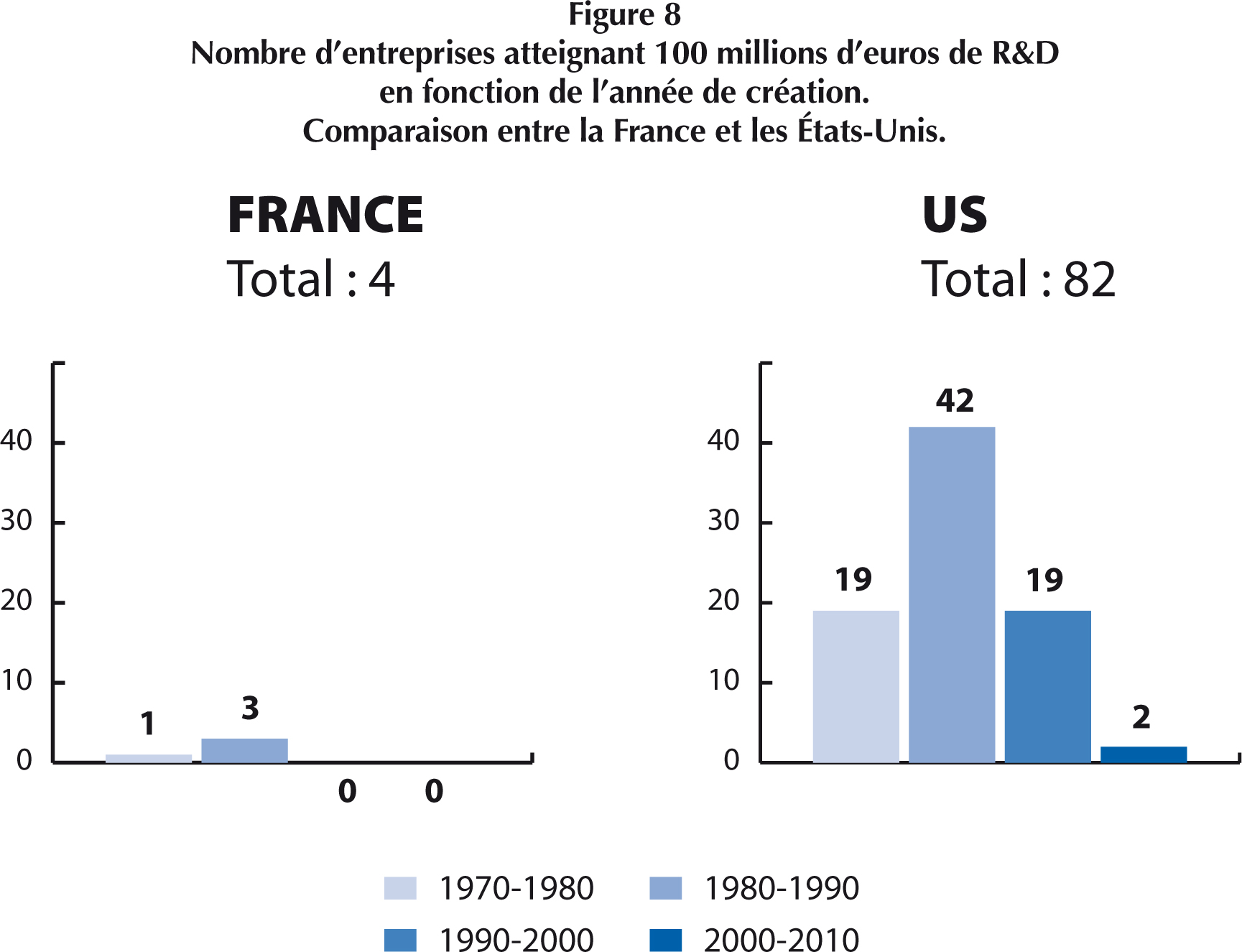

A real issue: company growth – number of companies reaching €100M in R&D relatively to company year of foundation

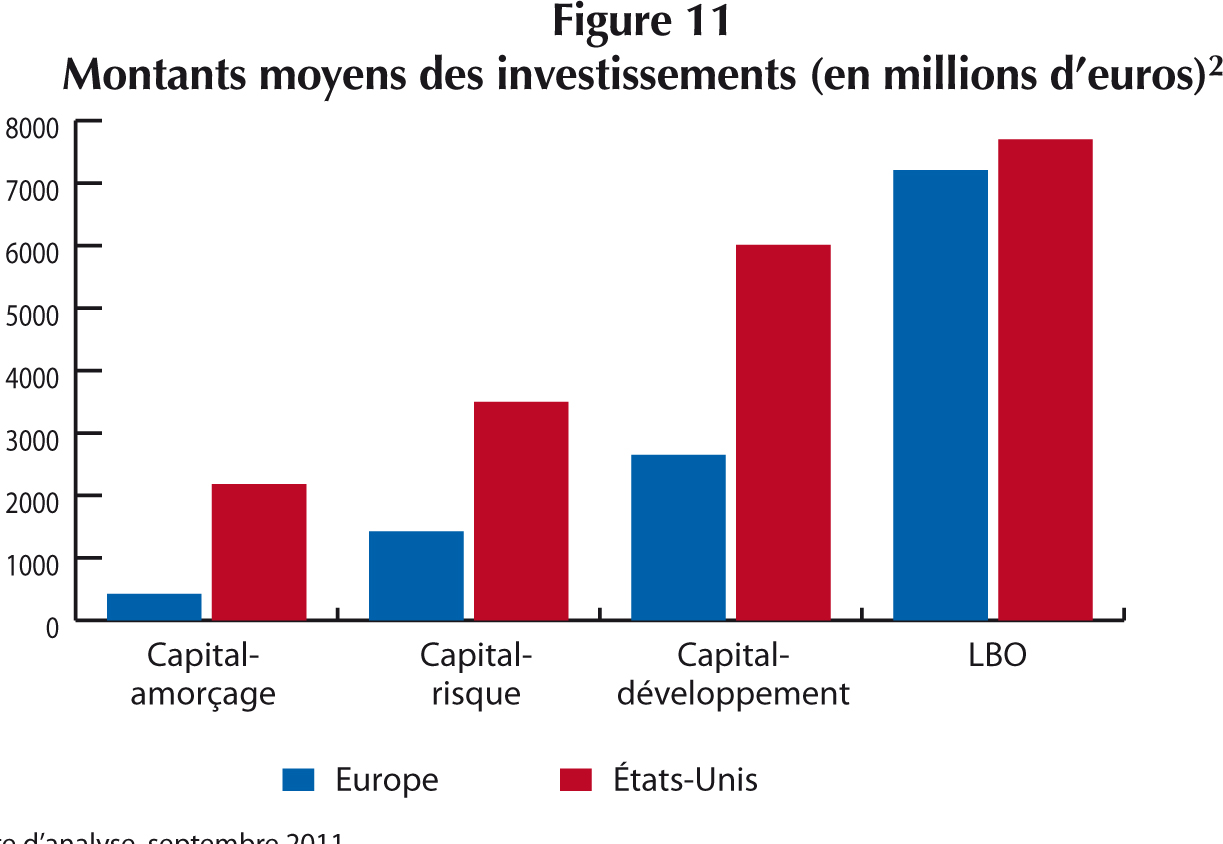

The complexity of the financing situation – as a % of GDP

The complexity of the financing situation – seed, early, late & LBO

As mentioned above this is the origin of 27 members (two presidents, 25 experts).

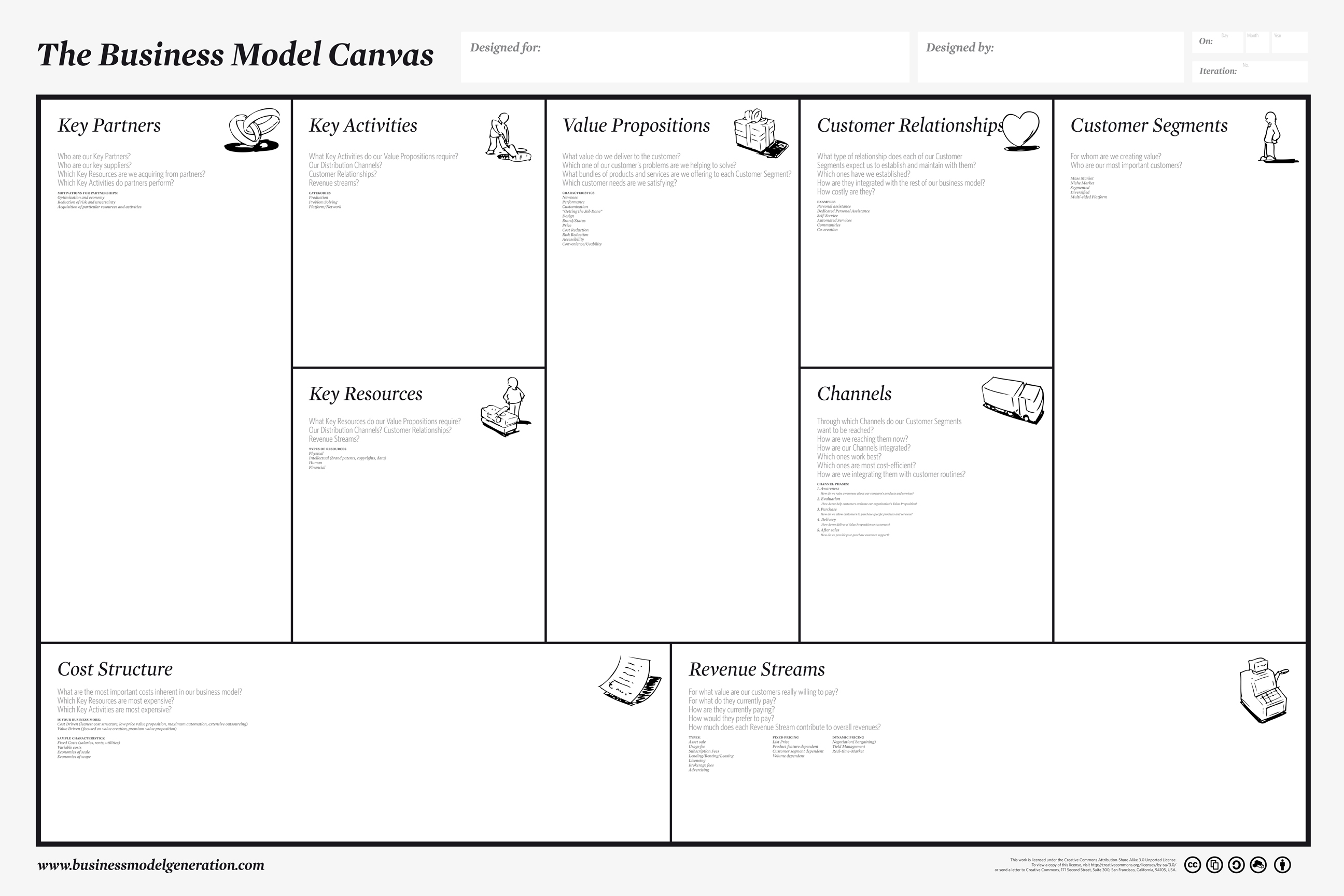

Last week, I attended a workshop organized by Raphael Cohen. He explained his IpOp process. You can read again the post I wrote a few months ago: Proven Tools for Converting Your Projects into Success (without a Business Plan). It’s really a good tool if you need to develop your own project. Cohen mentioned the famous Business Model Generation by Alexander Osterwalder and Yves Pigneur; and he showed us again its 9 building blocks. It has become such a standard… I never mentioned it here. Better late than never!

Very interesting presentation by the newspaper Le Temps and Xavier Comtesse about innovation in Switzerland (compared to the USA). (Thanks to Pascal for giving me the link :-)). The article is entitled The Swiss innovation model is it the best? (Same document on Prezi)

Before you view or read the content of the contribution by Comtesse, here is my reaction: it is indeed an excellent analysis, but the conclusion can be misleading! One could get the impression that the U.S. does not have large innovative companies like Switzerland has with Novartis, Roche or Nestlé. But I fear that it is a misleading view. The U.S. does not have that start-ups only and our are not growing. Not to forget, the topic of job creation, see Job creation: who’s right? Grove or Kauffman

Now here is a summary translated from Prezi: For several years, Switzerland has been at the top of the world rankings for innovation, this was not always the case especially during the 90s. So … Are we better than Silicon Valley?

Silicon Valley has developed a model in 8 strengths

– Excellent local university system

– Transfer of knowledge to the economy – technoloy parks, coaching, awards, etc..

– Powerful venture capital

– Start-ups that grow quickly and innovate in disruptive fields

– An effective IPO or M&A market (Exit Strategy)

– Large expenditures in R&D

– A high rate of patents per capita

– A strong entrepreneurial spirit per inhabitant

The 7 strong points of the Swiss model: Switzerland has a very different system of innovation from Silicon Valley but ultimately just as effective, especially for large companies.

– No federal masterplan for Innovation

– A concentration in life sciences

– A innovation driven by large companies

– Incremental innovation more than disruptive

– A quality education at all levels

– Framework conditions very favorable to the economy

– A high performance system of transfer of knowledge / technology

What are the strengths and weaknesses of Switzerland?

– Yes, our universities are excellent:

More than half of young Swiss university follow the one hundred best universities in the world, no country has such a result

– No, the Venture Capital industry is very low in Switzerland:

Switzerland underperformed largely in the area of venture capital (investment in Switzerland in 2011: 737 Million for USA 29,500 million).

– No, our start-ups do not grow fast enough:

The excellent survival rate is suspect, this means that start-ups are protected by the academic system or federal funding

– No, there is little IPO in Switzerland:

A small number of IPO (Initial Public Offering) shows weak growth start-ups or SMEs in Switzerland

– Yes, private R&D is very important but for large firms rather than in SMEs:

The share of the private sector is very important in Switzerland, particularly in the life sciences (pharma, biotech and medtech, etc.).

– Yes, we file a lot of patents:

but again it is primarily large enterprises, the proportion of patents is very important in Switzerland, this is partly due to the strong presence of very large firms

– No, the Swiss create firms twice less than the US:

the ntrepreneurial culture is very strong in the U.S., more than double that in Europe,

– Yes, the general conditions of business creation are very favorable:

Switzerland does better than innovative small countries such as Finland, Sweden and Israel

– Yes, technology transfer takes place in Switzerland:

Switzerland has fifty incubators, TechnoParks or other transfer centers Switzerland Silicon Valley

These two models as we have seen are very different. They work well both but the objective differences do not make possible to compare them as is done ll too often, especially in the field of start-ups …

2- Something Ventured, one of my favorite documentary on the topic. I mentioned already here: Something Ventured: a Great Movie and I show ti to my students as often as I can!

Here’s probably one of the toughest post I ever had to write and I am not sure it is a good one, even if the topic I am addressing is great and important. But it’s been a challenge to summarize what I learnt: Nicholas Nassim Taleb gives in this follow-up to the Black Swan a very interesting analysis of how the world can be less exposed to Black Swans, not by becoming more robust only, but by becoming antifragile, i.e. by benefiting from random events. His views include tensions between the individual and the groups, how distributed systems are more robust than centralized ones, how small unites are less fragile than big ones. This does not mean Taleb is against orgamizations, governments or laws as too little intervention induces totally messy situations. It is about putting the cursor at the right level. Switzerland represents for Taleb a good illustration of good state organizations with little central government, a lot of local responsibility. He has similar analogies for the work place, where he explains that an independent worker, who knows well his market, is less fragile to crises than big corporations and their employees. One way to make systems less fragile is to put some noise, some randomness which will stabilize them. This is well-known in science and also in social science. Just remember Athens was randomly nominating some of its leaders to avoid excess!

You can listen to Taleb here:

Now let me quote the author. These are notes only but for serious reviews, visit the author’s website, www.fooledbyrandomness.com/. First Taleb is, as usual, unfair but maybe less than in the Black Swan. Here is an example: “Academics (particularly in social science) seem to distrust each other, […] not to mention a level of envy I have almost never seen in business… My experience is that money and transactions purify relations; ideas and abstract matters like “recognition” and “credit” warp them, creating an atmosphere of perpetual rivalry. I grew to find people greedy for credentials nauseating, repulsive, and untrustworthy.” [Page 17] Taleb is right about envy and rivalry but wrong in saying it is worse in academia; I think it is universal! In politics for example. But when money is available, maybe rivalry counts less than where there is little.

Now a topic close to my activity: “This message from the ancients is vastly deeper than it seems. It contradicts modern methods and ideas of innovation and progress on many levels, as we tend to think that innovation comes from bureaucratic funding, through central planning, or by putting people through a Harvard Business School class by one Highly Decorated Professor of Innovation and Entrepreneurship (who never innovated anything) or hiring a consultant (who never innovated anything). This is a fallacy – note for now the disproportionate contribution of uneducated technicians and entrepreneurs to various technological leaps, from the Industrial Revolution to the emergence of Silicon Valley, and you will see what I mean.” [Page 42] [Extreme and unfair again, even if not fully wrong!]

“The antifragility of some comes necessarily at the expense of the fragility of others. In a system, the sacrifices of some units – fragile units, that is, or people – are often necessary for the well-being of other units or the whole. The fragility of every start-up is necessary for the economy to be antifragile, and that’s what makes, among other things, entrepreneurship work: the fragility of the individual entrepreneurs and their necessarily high failure rate”. [Page 65] What surprised me later is that Taleb shows that this is true of restaurants (not many succeed) as much as of high-tech start-ups. So it is not only about the uncertainty of new markets, but about uncertainty above all.

Mathematics of convexity

I have to admit Taleb is not easy to read. Not because it is complex (sometimes his ideas are pure common sense), but because it is dense with different even if consistent ideas. The book is divided in 25 chapters, but also in 7 books. In fact, Taleb insists on it, he might have written 7 different books! Even his mathematics is simple. His definition of convexity is a little strange though I found it interested (I teach convex optimization, and you might not know, it was the topic of my PhD!).

Jensen inequality is interesting [Pages 342, 227 – Jensen was an amateur mathematician!]– the convex transformation of a mean is less or equal than the mean after convex transformation. Again individual (concave, we die) vs. collective (convex, antifragile, benefits from individual failures). So risk taking is good for collectivity if with insurance mechanisms. Risk taking + insurance vs. speculation with no value added. An example of a short and deep idea: “Decision making is based on payoffs, not knowledge”. [Page 337]

“Simply, small probabilities are convex to errors of computation. One needs a parameter, called standard deviation, but uncertainty about standard deviation has the effect of making the small probabilities rise. Smaller and smaller probabilities require more precision in computation. In fact small probabilities are incomputable, even if one has the right model – which we of course don’t.” [Taleb fails to mention Poincare yet he quoted him in the Black Swan, but whatever.]

A visible tension between individual and collective interests

Quotes again: “What the economy, as a collective, wants [business school graduates] to do is not to survive, rather to take a lot, a lot of imprudent risks themselves and be blinded by the odds. Their respective industries improve from failure to failure. Natural and nature-like systems want some overconfidence on the part of the individual economic agents, i.e., the overestimation of their chances of success and underestimation of the risks of failure in their business, provided their failure does not impact others. In other words, they want local, but not global overconfidence”. […] In other words, some class of rash, even suicidal, risk taking is healthy for the economy – under the conditions that not all people take the same risks and that these risks remain small and localized. Now, by disrupting the model, as we will see, with bailouts, governments typically favor a certain class of firms that are large enough to require being saved in order to avoid contagion to other businesses. This is the opposite of healthy risk taking; it is transferring fragility from the collective to the unfit. […] Nietzsche’s famous expression “what does not kill me makes me stronger” can be easily implemented as meaning Mithridatization or Hormesis but it may also mean “what did not kill me did not make me stronger, but it spared me because I am stronger than others; but it killed others and the average population is now stronger because the weak are gone”. […] This visible tension between individual and collective interests is new in history. […] Some of the ideas about fitness and selection are not very comfortable to this author, which makes the writing of some sections rather painful – I detest the ruthlessness of selection, the inexorable disloyalty of Mother Nature. I detest the notion of improvement thanks to harm to others. As a humanist, I stand against the antifragility of systems at the expense of individuals, for if you follow the reasoning, this makes us humans individually irrelevant. ” [Pages 75-77]

A National Entrepreneur Day

“Compare the entrepreneurs to the bean-counting managers of companies who climb the ladder of hierarchy with hardly ever any real downside. Their cohort is rarely at risk. My dream – the solution – is that we would have a National Entrepreneur Day, with the following message: Most of you will fail, disrespected, impoverished, but we are grateful for the risks you are taking and the sacrifices you are making for the sake of the economic growth of the planet and pulling others out of poverty. You are the source of our antifragility. Our nation thanks you.” [Page 80]

Local distributed systems, randomness and modernity

“You never have a restaurant crisis. Why? Because it is composed of a lot of independent and competing small units that do not individually threaten the system and make it jump from one state to another. Randomness is distributed rather than concentrated.” [Page 98]

“Adding a certain number of randomly selected politicians to the process can improve the functioning of the parliamentary system.” [Page 104]

“Modernity is the humans’ large-scale domination of the environment, the systematic smoothing of the world’s jaggedness, and the stifling of volatility and stressors. We are going into a phase of modernity marked by the lobbyist, the very, very limited liability corporation, the MBA, sucker problems, secularization, the tax man, fear of the boss…” [Page 108]

“Iatrogenics means literally “caused by the healer”. Medical error still currently kills between three times (as accepted by doctors) and ten times as many people as car accidents in the United States, it is generally accepted that harm from doctors – not including risks from hospitals germs – accounts for more deaths than any single cancer. Iatrogenics is compounded by the “agency problem” which emerges when one party (the agent) has personal interested that are divorced from those of the one using his services (the principal). An agency problem is present with the stockbroker and medical doctor whose ultimate interest is their own checking account, not your financial and medical health.” [Pages 111-112]

Theories and intervention.

“Theories are super-fragile outside physics. The very designation “theory” is even upsetting. In social science, we should call these constructs “chimeras” rather than theories. [Now you understand why Taleb has many enemies.] A main source of the economic crisis started in 2007 in the Iatrogenics of the attempt by […] Alan Greenspan to iron out the “boom-bust” cycle which caused risks to go hide under the carpet. The most depressing part of the Greenspan story is that the fellow was a libertarian and seemingly convinced of the idea of leaving systems to their own devices; people can fool themselves endlessly. […] The argument is not against the notion of intervention; in fact I showed above that I am equally worried about under-intervention when it is truly necessary. […] We have a tendency to underestimate the role of randomness in human affairs. We need to avoid being blinded to the natural antifragility of systems, their ability to take care of themselves and fight our tendency to harm and fragilize them by not giving them a chance to do so. […] Alas, it has been hard for me to fit these ideas about fragility within the current US political discourse. The democratic side of the US spectrum favors hyper-intervention, unconditional regulation and large government, while the Republican side loves large corporations, unconditional deregulation and militarism, both are the same to me here. Let me simplify my take on intervention. To me it is mostly about having a systematic protocol to determine when to intervene and when to leave systems alone. And we may need to intervene to control the iatrogenics of modernity – particularly the large-scale harm to the environment and the concentration of potential (though not yet manifested) damage, the kind of thing we only notice when it is too late. The ideas advanced here are not political, but risk-management based. I do not have a political affiliation or allegiance to a specific party; rather, I am introducing the idea of harm and fragility into the vocabulary so we can formulate appropriate policies to ensure we don’t end up blowing up the planet and ourselves.” [Pages 116-118]

“To conclude, the best way to mitigate interventionism is to ration the supply of information. The more data you get, the less you know.” [Page 128]

“Political and economic “tail” events are unpredictable and their probabilities are not scientifically measurable.” [Page 133]

The barbell strategy and optionality

“The Barbell strategy is a way to achieve anti-fragility, by decreasing downside rather than increasing upside, by lowering exposure to negative Black Swans. So just as Stoicism is the domestication, not the elimination, of emotions, so is the barbell a domestication, not the elimination, of uncertainty.” [Page 159] “It is a combination of two extremes, one safe and one speculative, deemed more robust than a monomodal strategy. In biological systems, the equivalent of marrying an accountant and having an occasional fling with a rock star; for a writer, getting a stable sinecure and writing without the pressures of the market. Even trial and error are a form of barbell.” [Glossary page 428]

“The strength of the computer entrepreneur Steve Jobs was precisely in distrusting market research and focus groups – those based on asking people what they want – and following his own imagination, his modus was that people don’t know what they want until you provide them with it.” [Page 171]

“America’s asset is simply risk taking and the use of optionality, the remarkable ability to engage in rational forms of trial and error, with no comparative shame in failing, starting again and repeating failure. In modern Japan, by contrast, shame comes, with failure, which causes people to hide risks under the rug, financial or nuclear.”

“Nature does a California-style “fail early” – it has an option and uses it. Nature understands optionality effects better than humans. […] The idea is voiced by Steve Jobs in a famous speech: “Stay hungry, stay foolish.” He probably meant “Be crazy but retain the rationality of choosing the upper bound when you see it.” Any trial and error can be seen as the expression of an option, so long as one is capable of identifying a favorable result and exploiting it.” [Page 181]

“Option is a substitute for knowledge- actually I don’t understand what sterile knowledge is, since it is necessarily vague and sterile. So I make the bold speculation that many things we think are derived by skill come largely from options, but well-used options, much like Thales’s situation [who had an option with olive presses – pages 173-174] rather than from what we claim to be understanding.” [Page 186]

Taleb is skeptical with experts, with anyone believing in a linear model academia -> applied science ->practice (“lecturing birds how to fly”); he believes in tinkering, heuristics, apprenticeship, and makes again many enemies for free! He claims the jet engine, financial derivatives, architecture, medicine were first developed by practitioners and then theorized by scientists, not invented or discovered by them.

Tinkering vs. research

“There has to be a form of funding that works. By some vicious turn of events, governments have gotten huge payoffs from research, but not as intended – just consider the Internet. It is just that functionaries are too teleological in the way they look for things and so are large corporations. Most large companies, such as Big Pharma, are their own enemies. Consider blue sky research, whereby grants and funding are given to people, not projects, and spread in small amounts across many researchers. It’s been reported that in California, venture capitalists tend to back entrepreneurs, not ideas. Decisions are largely a matter of opinion, strengthened with who you know. Why? Because innovations drift, and one needs flâneur-like abilities to keep capturing the opportunities that arise. The significant venture capital decisions were made without real business plans. So if there was any analysis, it had to be of a backup, confirmatory nature. Visibly the money should go to the tinkerers, the aggressive tinkerers who you trust will milk the option.” [Page 229]

“Despite the commercial success of several companies and the stunning growth in revenues for the industry as a whole, most biotechnology firms earn no profit.” [Page 237] [Optionality again]

“(i) Look for optionality; in fact, rank things according to optionality, (ii) preferably with open-ended, not closed-ended, payoffs; (iii) do not invest in business plans but in people, so look for someone capable of changing six or seven times over his career, or more (an idea that is part of the modus operandi of the venture capitalist Marc Andreessen); one gets immunity from the backfit narratives of the business plan by investing in people. Make sure you are barbelled, whatever that means in your business.” [Page 238]

“I did here just debunk the lecturing-Birds-How-to-Fly epiphenomenon and the “linear model”, suing simple mathematical properties of optionality. There Is no empirical evidence to support the statement that organized research in the sense it is currently marketed leads to great things promised by universities. [Cf also Thiel lamentations about the promise of technologies – https://www.startup-book.com/2010/10/12/tech-equals-salvation/ ] Education is an institution that has been growing without external stressors; eventually the thing will collapse.” [A conclusion to book IV, page 261]

Why is fragility non linear?

“For the fragile, the cumulative effect of small shocks is smaller than the single effect of an equivalent single large shock. For the antifragile, shocks bring more benefits (equivalently, less harm) as their intensity increases (up to a point).”

Via negativa

“We may not need a name for or even an ability to express anything. We may just say something about what it is not. Michelangelo was asked by the pope about the secret of his genius, particularly how he carved the statue of David. His answer was: It’s simple, I just remove everything that is not David.” [Page 302-304]

[…] “Charlatans are recognizable in that they will give you positive advice. Yet in practice, it is the negative that’s used by the pros. One cannot really tell if a successful person has skills, or if a person with skills will succeed – but we can pretty much predict the negative, that a person totally devoid of skills will eventually fail.”

[…] “The greatest – most robust – contribution to knowledge consist in removing what we think is wrong. We know a lot more what is wrong than what is right. Negative knowledge is more robust to error than positive knowledge. […] Since one small observation can disprove a statement, while millions can hardly confirm it [The Black Swan!], disconfirmation is more rigorous than confirmation. […] Let us say that, in general, failure (and disconfirmation) are more informative than success and confirmation.”

[Funnily, I remember the main critics against my book were the lack of [positive] proposal in the end. I should have said there we many about what not to do!]

“Finally, consider this modernized version in a saying from Steve Jobs: “People think focus means saying yes to the thing you’ve got to focus on. But that’s not what it means at all. It means saying no to the hundred other good ideas that there are. You have to pick carefully. I’m actually as proud of the things we haven’t done as the things I have done. Innovation is saying no to 1,000 things.” [Page 302-304]

Less is more

“Simpler methods for forecasting and inference can work much, much better than complicated ones. “Fast and frugal” heuristics make good decisions despite limited time. First extreme effects: there are domains in which the rare event (good or bad) plays a disproportionate share and we tend to be blind to it. Just worry about Black Swan exposures and life is easy. There may not be an easily identifiable cause for a large share of the problems, but often there is an easy solution, sometimes with the naked eye rather than the use of the complicated analyses. Yet people want more data to solve problems.” [Page 305-306]

“The way to predict rigorously is to take away from the future, reduce from it things that do not belong to the coming times. What is fragile will eventually break, and luckily we can easily tell what is fragile. Positive Black Swans are more unpredictable than negative ones. Now I insist on the via negativa method of prophecy as being the only valid one.” [Page 310]

“For the perishable, every additional day in the life translates into a shorter additional life expectancy. For the non perishable, every additional day may imply a longer life expectancy. On general, the older the technology, the longer it is expected to last. I am not saying that all technologies do not age, only that those technologies that were prone to aging are already dead.” [Page 319]

“How can we teach children skills for the twenty-first century, since we do not know which skills will be needed? Effectively my answer would make them read the classics. The future is in the past. Actually there is an Arabic proverb to that effect: he who does not have a past has no future.” [Page 320]

[As can be read later in the book Taleb does not like the Bay Area culture. And it is no coincidence, it is a region with nearly no past, nearly no history, but it certainly help it create Silicon Valley innovations…]

“If you have an old oil painting and a flat screen television, you will never mind changing the television, not the painting. Same with an old fountain pen and the latest Apple computer; [Taleb is really cautious with modernity and innovation, even if a user of it. With architecture, he has similar concerns. Again he prefers tradition to aggressive modernity. Same with the metric system vs. old methods] Top-down is usually irreversible, so mistakes tend to stick, whereas bottom-up is gradual and incremental, with creation and destruction along the way, thought presumably with a positive slope.” [Pages 323-24]

“So we can apply criteria of fragility and robustness to the handling of information – the fragile in that context is, like technology, what does not stand the test of time. […] Books that have been around for ten years will be around for ten more; books that have been around for two millennia should be around for quite a bit of time. […] The problem in deciding whether a scientific result or a new “innovation” is a breakthrough, that is, the opposite of noise, is that one needs to see all aspects of the idea – and there is always some opacity that time, and only time, can dissipate.” [Page 329]

“Now, what is fragile? The large, optimized, overreliance on technology, overreliance on the so-called scientific method instead of age-tested heuristics.”

“By issuing warnings based on vulnerability – that is, substractive prophecy – we are closer to the original role of the prophet: to warn, not necessarily to predict, and to predict calamities if people don’t listen.”

Ethics

“Under opacity and complexity, people can hide risks and hurt others. Skin in the game is the only true mitigator of fragility. We have developed a fondness for neomanic complication over archaic simplicity. […] The worst problem of modernity lies in the malignant transfer of fragility and antifragility from one party to the other, with one getting the benefits, the other one (unwittingly) getting the harm, with such transfer facilitated by the growing wedge between the ethical and the legal. Modernity hides it especially well. It is of course an agency problem.” [Page 373]

[You can/should have a look at table 7, page 377]

“In traditional societies, a person is only respectable and as worthy as the downside he (or, more, a lot more, than expected, she) is willing to face for the sake of others.” [Page 376]

“I want predictors to have visible scars on their body from prediction errors, not distribute these errors to society.” [Page 386]

[Don Quixote was already the sign of the end of the heroism, of the ethical behavior. Taleb’s models are Malraux and Ralph Nader – “the man is a secular saint” [Page 394]. His enemies Thomas Friedman, Rubin and Stieglitz]

[Is “skin in the game” the only way? The only solution? What about transparency?]

About Science

“Science must not be a competition; it must not have rankings – we can see how such a system will end up blowing up. Knowledge must not have an agency problem. One doctoral student once came to tell me that he believed in my ideas of fat tails and my skepticism of current methods of risk management, but that it would not help him get an academic job. “It’s what everybody teaches and uses in papers” he said. Another student explained that he wanted a job at a good university, so he could make money testifying as an expert witness – they would not buy my idea on robust risk management because “everyone uses these textbooks”. [Page 419]

“All I want is to remove the optionality, reduce the antifragility of some at the expense of others. It is simple via negativa. […] The golden rule: “Don’t do unto others what you don’t want them to do to you”. […] Everything gains or loses from volatility. Fragility is what loses from volatility or uncertainty. […] Time is volatility. Education in the sense of the formation of the character, personality, and acquisition of true knowledge, likes disorder; label-driven education and educators abhor disorder. Innovation is precisely something that grains from uncertainty.” [Pages 420-22]

“It so happens that everything nonlinear is convex, concave or both. […] We can build Black-Swan-protected systems thanks to detection of concavity, […] and with a mechanism called convex transformation, the fancier name for the barbell. […] Distributed randomness (as opposed to the concentrated type) is a necessity.”

[General comments]

Taleb sometimes gives the feeling of contradictions: marketing is bad, but Steve Jobs is great; barbell strategy and optionality is great, but isn’t it about risks and downsides transferred to others [Isn’t Thales a pure speculator?], cigarettes are bad but traditions are good.

Also this love of tradition makes people with more background at ease to take risks with barbell strategy; but what about the poor with nothing to lose? Benefits might statistically go to those who already have… [It reminds the story told by J.-B. Doumeng: It is a millionaire who recounts his difficult beginnings: “I bought an apple 50 cents, I polished it to shine and I sold it for one franc. With this, I bought two apples 50cts, I carefully polished and I sold them 2 Fr after a moment, I could buy a cart to sell my apples and then I made a big inheritance … “]

You now know why it has been a challenge. A very strange, dense, fascinating book, but if you like these concepts, you must read Antifragile. In fact you must read the Black Swan first, if you have not and if you like it, I am sure you will read Antifragile.

It begins with: “Try as you may, innovation can never be reduced to a mere good idea. Innovation is a process, which is played chiefly in the way those who are to implement it can successfully make novelty theirs. Quite often management tends to overlook this process of appropriation, or to consider it only in terms of hindrances and obstacles. How, on the contrary, can the internal resources of organizations be enhanced and mobilized? The answer is straightforward: by developing a culture of cooperation, which allows for some degree of transgression… and also makes way for emotion.”

A few more interesting ideas:

– “Firstly, we tend to confuse invention with innovation. An invention is the act of creating something new. As such, it may be the fruition of a single man’s ingenuity. Innovation, on the other hand, involves disseminating such novelty. It refers to a much broader process that includes social, economic and technological dimensions.”

– Then, a nice analogy quoting someone: “I hate GPS. When driving with a GPS, you don’t look at the landscape, you don’t notice the signs, and given you don’t get lost you don’t get to ask directions to others.”

– Finally, “innovators are always a minority, or at any rate that’s the way they start out, and the more allies you find in an innovative project, the better you bear with being a minority.”

This is my third article in the journal Entreprise Romande (and thank you to them for editing my work and for the opportunity given to talk about topics that are dear to me.)

Every entrepreneur knows that failure is an integral part of business: a contract breach, a lost customer, a unsatisfactory hire… So why is failure so stigmatized in the European culture, and especially in Switzerland? Freeman Dyson, ths famous physicist explains it more clearly: “You can’t possibly get a good technology going without an enormous number of failures. It’s a universal rule. If you look at bicycles, there were thousands of weird models built and tried before they found the one that really worked. You could never design a bicycle theoretically. Even now, after we’ve been building them for 100 years, it’s very difficult to understand just why a bicycle works – it’s even difficult to formulate it as a mathematical problem. But just by trial and error, we found out how to do it, and the error was essential.” The example of the bicycle is just perfect: who would blame a young child for his multiple drops wjile learning who to ride it?

FAILURE AND CREATIVITY

Silicon Valley is known for its tolerance for failure, which, far from being a stigma, is even valued. “In Silicon Valley, if we had not tolerated failure, we would not be able to take risks and we would have many fewer entrepreneurs than we have today. If you fail for good reasons, that is to say almost all, except to be corrupt, stupid or lazy, then you have learned something that will make you more useful,” says Randy Komisar, based in Silicon Valley, as are the other people mentioned in this article. “You’d be amazed at how many investors prefer to back someone who has tasted the bitter fruits of failure. In failing you learn what not to do. Get your skin in the game and there is no failure—you have opened your mind to growth and yourself to reinvention,” adds Larry Marshall.

The fear of failure has deep roots. The school system encourages the child not to try or say anything if she does not know the answer rather than testing hypotheses, for fear of reprimand. Experimentation, creativity, the “process of trial and error”, are never quite encouraged in favor of more rational disciplines. “Indeed, we have psychological and intellectual difficulties with trial and error and with accepting that series of small failures are necessary in life. “You need to love to lose”. In fact the reason I felt immediately at home in America is precisely because the American culture encourages the process of failure, unlike the cultures of Europe and Asia where failure is met with stigma and embarrassment”, says Nicolas Taleb, essayist of Lebanese origin and writer of The Black Swan.

The European start-ups do not fail! Their survival rate is 90% after 5 years of existence. But is it good news? In the first months of Google,co- its founder Larry Page considered a success rate of 70% of individual projects was ideal. Asking for more, “we would take too few risks.” And failure is so digested that Americans have created the FailCon (a conference on failure) in 2009. By sharing their experience of failure in public (because failure is still a taboo even in the United States), participants learn from their peers and leave strengthened. The famous entrepreneur and investor Vinod Khosla admitted to have failed more often than he was successful. “Failure is not desirable, it is just part of the system, and it is high time to accept it.” Would this explain why we do not create any Google Switzerland and Europe?

PREPARING FOR SUCCESS

Nevertheless, the failure will always be unpredictable. “Of course, business, just as life, is never a smooth curve. Failure can come as quickly, and more unexpectedly, as success. But true success is management of failure. Every time you hit a bad patch you must be able turn your fortunes around. That’s why it’s important to be always prepared for failure and build strong teams. To be a successful entrepreneur, venture capitalist or philanthropist, you must bring together people who know there will be problems, love to solve problems, and can work well as a team.” … “It reminds me not to be too proud. I celebrate failure — it can temper your character and pave the way for great achievement.” notices Kamran Elahian.

So, should we be not afraid to fail? A short and most moving answer comes from Steve Jobs, who – we must not forget – failed to grow Apple in the 1980s: “I didn’t see it then, but it turned out that getting fired from Apple was the best thing that could have ever happened to me. The heaviness of being successful was replaced by the lightness of being a beginner again, less sure about everything. It freed me to enter one of the most creative periods of my life.” And even better: “Remembering that I’ll be dead soon is the most important tool I’ve ever encountered to help me make the big choices in life. Because almost everything — all external expectations, all pride, all fear of embarrassment or failure – these things just fall away in the face of death, leaving only what is truly important. Remembering that you are going to die is the best way I know to avoid the trap of thinking you have something to lose. You are already naked. There is no reason not to follow your heart.”

When will a FailCon be organized in Switzerland?

A Chinese student introduced me to a few years ago the following proverb: “Shi Nai Bai Zhi Gong Cheng Mu”, which means “failure is the mother of success.” Asia might learn perhaps faster than Europe this important concept.

As much for my personal archive (a blog is a second brain!), as for you, the reader, the Swiss-German TV broadcast, “ECO” (the weekly economic magazine on SF1), talked about French-speaking Swiss start-ups at EPFL.