HBO’s Silicon Valley season 4 ended a few weeks ago. And there will be a season 5 in 2018. This was not the best one but I still like it. In the last episode, our heroes struggle and meditate…

HBO’s Silicon Valley season 4 ended a few weeks ago. And there will be a season 5 in 2018. This was not the best one but I still like it. In the last episode, our heroes struggle and meditate…

A tribute to Maryam Mirzakhani

From time to time, I mention here books about science and mathematics that I read. It is the first one I read by Ian Stewart. Shame on me, I should have read him a long time ago. 17 Equations That Changed the World is a marvelous little book that describe the beauty of mathematics. A must read, I think

So as a little exercise, you can have a look at these 17 equations and check how much you know. What ever the result, I really advise to read his book! And if you do not, you can have a look at the answers below…

And here is more, the names of the equations and the mathematitians who who discovered them (or invented them – depending on what you think Math is about).

I publish more and more posts about politics, society and start-ups. I recently had one about sexism in Silicon Valley and the motivation for this one is a French blogger who critized French president, Emmanuel Macron, for his saying that France should become a startup nation. The author, Mehdi Medjaoui, reacted by writing Non, la France ne doit pas devenir une start-up (No, France must not become a start-up).

This is a very interesting article in French, so I put most of the content in Google Translate and though I did my best to correct this (decently good) tool, I am not sure what follows is easily readable. But the main messages should be possible to follow. It is worth the read. the author knows very well start-ups and Silicon Valley and he does not have (I think) really much against them, btu I agree with him, their unique model and dynaics cannot and should be copied by states, and indeed only by a tiny number of people or groups.

No, France is not a start-up, that is to say a temporary organization in search of a model of growth and income, as defined by Steve Blank, one of the pioneers to theorize the mentality start- Up in Silicon Valley. France is a multi-century nation, whose model of “freedom equality fraternity” is universal, universalist and resonant for eternity. She is no longer looking for a model. She has been in the execution of this model for 220 years.

No, France is not a start-up, owned by a small number of shareholders and unelected investment funds, authorized to make unilateral choices without counter-measures that are necessary for the whole group. France is a democratic, sovereign nation whose representatives are of the people, elected by the people, for the people and seeking the separation and balance of power in the interests of all these citizens.

No, France should not think “make something people want”, as would say Paul Graham, the founder of the best-known start-up accelerator that is YCombinator. France is a Republic (res-publica, the public thing) which thinks the general interest over particular interests. We would still have the death penalty if we were content to accomplish only the things people wanted. France must think “make what the people want”. The people as a whole. Not a part of the people.

No France should not adopt the strategy of blitzscaling thought by Reid Hoffman – founder of LinkedIn and investor – that is to say to invest resources with very great loss, on a very risky profile, betting on the debt to take Dominant market positions. France must manage its public finances in good faith because it is fundamentally the money of the citizens, and it must invest in infrastructure for the future, less risky and less profitable in the short term. It is not for the French State to take risks, it is for entrepreneurs, who will be rewarded for this. Because yes, thinking like a start-up is thinking of extreme growth, at any price, in a leak forward that leads to failure in 90% of cases. But unlike a startup, if you miss, you cannot start France again.

No, France must not succumb to the dictatorship of innovation that prevails in Silicon Valley, which is beginning to innovate to innovate as long as there are people to invest in a bubble economy … As Peter Thiel would say in “Where is the Future”. “We wanted flying cars, we had networks of 140 characters instead.” France should not think and control itself like a game where one bursts of candy, or a social network of photos or micro-messaging.

“France, the 5th world power and nuclear power does not drive like CandyCrush, Tinder or Snapchat”

On the other hand, France must think Progress. With values from the Enlightenment, it must enlighten the world again by thinking about the future, and by putting innovation and start-ups at the service of this future, because “Innovation without conscience is only ruin of the soul”.

For example, France as a nation must think the future by its ethical scientific and industrial intellectuals, define qualitative and quantitative objectives for the future of humanity, encourage innovation in this direction, go out of the «spray and pray» which is to believe that we must water and support all innovations and pray to see those that will evolve in progress.

It can do this by piloting its public research towards these objectives, the steering of its policy of financing innovation through the Public Investment Bank and the Caisse des Depots et Consignations and an open policy of valorization by its Socities for the Accelerated Transfer of Technology (SATT). The state can also do so with the legal context of intellectual property to allow all entrepreneurs in the territory to have a free license on unused patents owned by the state.

It is perhaps even negotiating at the global level to renounce the patenting of living organisms or medicines for poorer countries, or clean energy, in a logic of progress for humanity against the logic of capital. Somewhat like Elon Musk did when he put Tesla’s patents in the public domain, or the YCombinator accelerator I mentioned earlier, which guarantees with its YCResearch research center that all the results from their Works will be in the public domain.

At the same time, France, unlike the start-up philosophy, has to direct the world to think about the crazy guards that innovation tries to circumvent pushed by its logic of short-term profit. For example, Silicon Valley entrepreneurs and researchers in the OpenAI movement want to finance the balance of knowledge in the field of artificial intelligence to ensure that it does not drift and becomes our last invention. It is the role of an enlightened nation like France to think these things on a global level. Not to think like a start-up to accept any innovation whatever its impact on the world, on the sole pretext that it is innovation, without knowing in which direction to go. For as the Chinese proverb says, “There is good wind only to him who knows where he is going”.

No France should not yield like start-ups to the galactic datacracy which thinks that one can control everything with metrics of acquisition, activation, retention, income and recommendations, statistics and the Big data. Or even succumb to what Eric Ries, the author of Lean Startup, calls the Vanity Metrics, these indicators of success that are not. That we can all automate, in a virtuous martingale this creation of value and unlimited. No, the data is only a representation of reality because it always suffers from statistical and collection bias. As Jacky Fayolle, administrator of INSEE, puts it: “When indicators are used in a fetish fashion, disconnected from the information system from which they come, they deplete public action rather than enrich it, while Offering an easy but illusory assessment of the performance of these actions.”

Cathy O’Neil in her book Weapons of Maths Destruction: How Big Data Increases Inequality and Threatens Democracy takes on the example of the subprime crisis Where she explains that “a formula can be perfectly innocuous in theory. But when it is used on a large scale and becomes a national or global standard, it creates its own distorted and dystopic economy.” Behind, these are not application features that no longer work, they are people expropriated and put On the street, the financial bankruptcies of people who had invested their retirement in the markets and who have nothing more … and public money by hundreds of billions of all the citizens who come to bail out the banks.

On the scale of a start-up looking for its model, it is easy to go back in the real to understand what is not working and to publish a new version of the software two days later. When one speaks of basing the whole society behind the data, one takes the risk of diluting its meaning, which creates a systemic risk of discrepancy between reality and its statistical or algorithmic representation on a scale where one does not Can stop the machine.

No, France should not “Move fast and break things”, that is to say to innovate at the risk of breaking the existing, as Mark Zuckerberg said in the first ten years of Facebook. France must guarantee national cohesion, guaranteeing progress for all, in the long term and without breaking the gains of social progress, its culture and its living together which are a legacy of the common French. Moreover once a critical size reached for Facebook, Mark Zuckerberg changed this principle to “Move fast with stable infrastructure”. This is closer to a sound strategy of rapid development by respecting the stability of what has already been built before, and which endorses the fact that Facebook was no longer a start-up. As France, too, must not think as such, it must also maintain the stability of its infrastructures, as quickly as it moves.

No, France does not have to “Fuck it, ship it”, an ideology that promotes the release of products not yet finished, to confront them with reality and learn from their impact on customers and the market. As Reid Hoffman (again) says, “If you’re not ashamed of your product when you take it out, it’s because you took too long to get it out and you’d have to get it out a lot sooner”.

France must think about reforms and laws in a spirit of respect for institutions, debate and consultation in the constitutional requirement and not produce laws or any other reform or infrastructure, without thinking about equality of rights. When you manage 67 million people in such an advanced way in your life, you cannot produce laws, utilities, infrastructure without thinking for all in the long run. You cannot do it without planning them on qualitative and quantitative goals of progress, egalitarian and ecological, just to get them out and see what it gives and then iterate. In other words: motorways or nuclear power plants are not built in “Fuck it ship it” mode.

No, France should not “Ask for forgiveness, not for permission”. The acts of the French state bind him before history. This can be seen, for example, in Germany, which still has no right to hold nuclear weapons or Japan which cannot devote more than 1% of its GDP to its army in retaliation for their actions during the second world War. It can also be seen with the consequences of colonization which remain open wounds in a large part of the population and a French dishonor in the History of the world. A start-up can make moral mistakes, play with the limits of the law like Uber and Airbnb to move the lines, but a state has many other responsibilities of another kind before international law and the course of the story. No France ought not to engage the nation for the future without thinking of the consequences.

France does not have to fail fast, fail often, but France is a nation state whose model has no right to break, in a country with 9 million poor people, 4 million poorly housed. Moreover, France cannot economically go bankrupt. The economic defeat, it ends in the end by “hyperinflation or war” as Karl Marx would say. Hyperinflation if we try to pay off the debts that have become un-repayable, the war with its creditors if we do not want to pay them back and they come to force it back.

And then we cannot start France again with another team and other investors. There is but one people of France, and one territory of France.

No France should not like a start-up segment its offers according to the citizens in a cleaving relationship, for citizens who can afford to subscribe and others not. On the contrary, it must treat the whole territory and all its citizens in an inclusive, “equal with equals, unequal with unequal” way, to compensate for differences of fact or nature, not to accentuate them.

No France should not invest everything solely on technological solutionism, which advocates that everything can be solved with an application, as Evgeny Morozov explains in his book “To save everything click here” or Jaron Lanier in his book “Who owns The Future.” Things are more complex than that when you run a nation. France must think, like Barack Obama in front of Silicon Valley entrepreneurs, that “Democracy is by definition disordered and that if all I had to do was produce a widget (web or mobile application) without worrying about Whether the poorest can access it or worry about possible collateral damage, then the recommendations of the Silicon Valley bosses would be great.”

No, France should not create temporal monopolies, as Peter Thiel would say in his book Zero to One, in order to create more margin than its competitors (especially Europeans) in order to continue investing to maintain this monopoly. France needs to think of economic collaboration with its European partners, to rebuild a political Europe that goes beyond the doctrine of free and undistorted competition that puts countries in tax and social competition. France must establish itself in Europe in a logic of cooperation, as we have seen with the industrial successes of Airbus and Ariane Espace. There remain the economics of the sea, the digital and so many other areas on which to cooperate at the European level with our partners, not our competitors.

Instead of being a start-up and thinking like a start-up, France must become an entrepreneurial state. In this context, its role is a regulator, an insurer of last resort and an arbitrator who ensures the freedom to undertake, reduces the opportunity cost and the cost of access to the market to its minimum for entrepreneurs , Helps finance innovation, supports basic research, while protecting its strategic industries. Its role is to ensure neutrality, equity, transparency and stability in the marketplace to create a climate of sound confidence and enable entrepreneurs to innovate. In this respect, it is concretely to create an infrastructure favorable to the creation of value, with maximum positive externalities to allow the emergence of a fertile ecosystem to the taking of risk. But it is not France that must take risks! Entrepreneurs will be more agile to identify market needs and build experiences that customers expect. The State is involved in investing in infrastructure over the long term and pooling them for all, with access costs tending to zero with the number, allowing the opportunity cost to the entrepreneurial Real equality of opportunity.

So it is not to think like a start-up but to think like an infrastructure that allows the emergence of startups, guaranteeing as a state the counterpart of the legislative framework in the direction of Progress over the long term for the society.

A State is the opposite of “move fast and break things”, but rather “move forward and do not break”

“We can not stop progress” or the dictatorship of innovation

“In the speech of Emmanuel Macron at Vivatech, the word innovation is pronounced 25 times, the word progress does not appear.”

As Etienne Klein has often said in his lectures, “50 years ago, for every innovation that brought society forward, it was said, We do not stop progress”. There was a benevolent vision of innovation where it was said that technology came to free men and women from their condition. In a society where innovation is king, this expression takes a whole different turn. “One does not stop progress” is today the expression of a dictatorship of innovation. Technology is seen as a bulimic monster that will come to threaten our future, take jobs, consume more resources, with no safeguards. It is the theories of the Singularity University in Mountain View, where it is believed that technology will replace the man in a “forced march” and make it obsolete.

Is this really our plan for the future?

“The idea of progress was a doubly consoling idea. In the first place, because by sustaining the hope of a future improvement of our living conditions, by making a more desirable world a long way off, it made history humanly bearable. Second, because it gave meaning to the sacrifices it imposed. In the name of a certain idea of the future, mankind was called upon to work for a progress which the individual would not necessarily Experience, but whose descendants could benefit. ”

In short, to believe in progress was to accept the sacrifice of the personal present in the name of a certain credible and desirable idea of the collective future. But for such a sacrifice to have any meaning, a symbolic attachment to the world and its future was required. Is it because such a connection is lacking today that the word progress is disappearing or curling up behind the single concept of innovation, now on the agenda of all research policies? ”

The idea of progress is the opposite of the start-up philosophy that runs in the short term, in a forward flight dictated by the dogma of innovation at all costs in the name of the market, without putting it in context Desire for the future. Not every innovation that meets a market is progress. Some examples? Allowing to share photos that fade on a social network is not a progress for humanity. Paying to choose the genetic characteristics of one’s children, is not a progress for humanity. Transplanting the blood of young adults to try to get younger rich businessmen to rejuvenate is not a progress. Allowing to meet men and women on a simple thumb on her phone is not a progress for humanity. It’s up to you to judge for yourself.

For all these reasons, France should not become a start-up, nor should it think and act as a start-up. France is a nation, a state, a people, a history, a culture that has to extricate itself from the permanent pivot, for it is capable of thinking the future in the name of a desirable idea for which its people are ready to sacrifice. These reversals of strategy startups who do not know where they go and what their model are the opposite. The French model is established “Liberty, Equality, Fraternity” and it has an eternal vocation, for France is not and will never be an enterprise, it is a Republic.

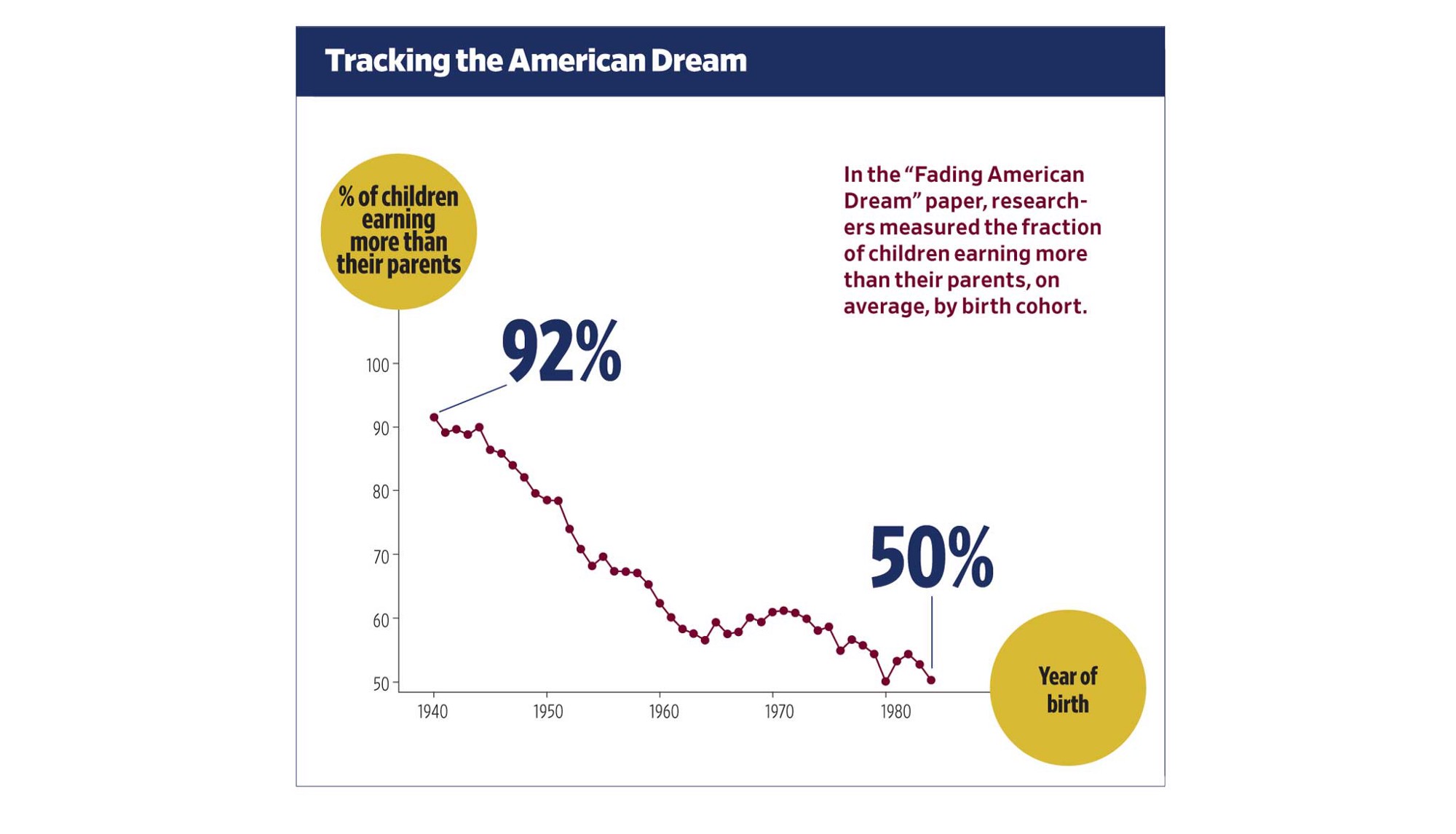

As I am a big fan of both Piketty and Harari in addition to being a start-up fan, I was attracted by this article from the Stanford Magazine: This is Not Your Parents’ Economy – Inequality is putting the American Dream in peril. Here is the most striking message:

According to the “Fading American Dream” paper, 92 percent of people born in 1940 earned more in income at age 30 than their parents did at age 30. Only 50 percent of those born in 1984 did.

[…]

In trying to explain why mobility has fallen so precipitously, Chetty, Grusky and their team considered two “counterfactual” scenarios for those born in the 1980s. The first assumes higher GDP growth, equivalent to that experienced by those born in 1940 but distributed as it has been recently. The second uses the real GDP growth for the 1980s cohort but assumes a “more broadly shared” distribution. As the paper explains, “the first scenario expands the size of the economic pie, dividing it in the proportions by which it is divided today. The second keeps the size of the pie fixed, but divides it more evenly as in the past.”

[…]

The higher GDP growth scenario did increase mobility — to 62 percent from 50 percent. But the more broadly shared growth scenario did even better, increasing mobility to 80 percent. To achieve that higher level of mobility using GDP alone would require growth of 6.4 percent per year. (Recent years have seen growth under 3 percent in the United States.)

[…]

“We were able to say, if you care about upward mobility, aggregate growth wouldn’t be enough to restore it; instead, growth needs to be more equitably distributed.”

Silicon Valley is talking these days a lot about sexism and harrassment. If you have nmot heard botu it yet, you may just want to read:

– Women in Tech Speak Frankly on Culture of Harassment from the New York Times, dated June 30, 2017.

– Uber’s Opportunistic Ouster in the New Yorker, dated July 10.

I have already mentioned here some dark features of Silicon Valley. For example:

– Is Silicon Valley crazy (again)? in January 2016,

– Something rotten in the Silicon Valley kingdom? in January 2014,

– Silicon Valley and (a)politics – Change the World in NOvember 2013,

There is no doubt Silicon Valley is not a paradise. But i had never seen it as a sexist place. At least not more sexist thn the rest of the planet. And yes, there has been terrible stories, such as rapes on the Stanford campus, but my recollection of the area is more of an asexual place, mostly of introvertite people, like you could see on HBO’s Silicon Valley (right from its 1st episode). Just read (again?) the funny and sad comment: “That’s weird, they always travel in groups of 5, these programmers. There is always a tall skinny white guy, a short skinny asian guy, a fat guy with a ponny tail, some guy with crazy facial hair, and then an east indian guy. It’s as if they trade guys until they have the right group.

– You clearly have a great understanding of humanity.”

But if there is something ot be said about all this, is that hwoever complex a society is and it is never easy to explain human interactions without being simplistic, what some and maybe too many individuals are doing in Silicon Valley is unacceptable and should be fought so that it happens less and less often…

Sorry – this should have been on the French version of my blog. I keep it there and copy it also on the FR side…

C’est en recevant ce matin un lien d’un article du journal de libération en date du 29 juin 2007 (vous lisez bien, 2007, pas 2017) que j’ai décidé de ce post. L’article s’intitule L’iPhone, sans mobile apparent. Il montre de manière presque hilarante la difficulté de prédire. Alors j’en ai profité aussi pour mettre sur Slideshare une présentation que j’ai faite il y a quelques jours intitulée les défis de l’innovation. Désolé car il n’y a pas l’audio, mais il y a quelques données révélatrices… enfin je crois…

Voici donc quelques extraits de l’article. Sur le marché du mobile tout d’abord: “Apple est modeste. Il ne vise que 1 % du marché du mobile, et ne pense écouler que 10 millions d’iPhones d’ici à la fin de 2008. Le marché du mobile, lui, tourne autour du milliard d’unités écoulées en 2006. […] Un créneau que Nokia a l’intention de solidement occuper. Sur les 350 millions de mobiles Nokia écoulés dans le monde en 2006, 77 millions sont des téléphones baladeurs capables comme l’iPhone de diffuser de la musique. Le finlandais a une bonne longueur d’avance…” Sur les chances d’Apple: “De l’avis des analystes, l’iPhone ne va pas bousculer le jeu.” […] «Apple, en lançant son iPhone, est sur le mode défensif. Il n’avait pas vraiment le choix.» 🙂

Voici donc mes slides. Je vous conseille les slides 6 et 10 de la partie 1, la partie 2 est un recyclage de présentations passées, que j’aime aussi tout particulièrement…

There is no doubt about it, and as the summer begins smoothly, I allow myself an article somewhat less serious than usual, which confirms the thesis of my previous article, The University-based Startup Porsche Principle. Or is it the Tesla Principle?

Innovation is a complex topic but this does not prevent the desire to measure it. The Global Innovation Index with its 83 parameters is the best illustration of this. But cann’t we make it simpler? I propose the simpler Tesla Index which measures the number of Tesla linked to the institution which innovation is to be measured. It shows a certain financial success combined with a curiosity for novelty. We can always bring it back to the size of the entity if necessary …

At EPFL, the Tesla index according to my measures is 4 as of June 26, 2017 …

A Tesla, being charged on the EPFL campus on June 26, 2017…

on June 15, 2017

on June 13, 2017

on May 10, 2017

then the index goes up to 5, on July 4, 2017

then the index goes up to 7, on July 14, 2017 (I am not sure the red one is not the one I found first above). Thanks, Aurélien!

I usually do not mix my EPFL activity and my blog activity. This is one of the rare exceptions. At EPFL’s startup unit, we just published a short report describing EPFL spin-offs. Here is a short link. By the way you can also visit the pages about EPFL’s support to entrepreneurship.

The report gives data about value creation through fund raising and job creation and also about a known phenomenon, the importance of migrants for entrepreneurship. I am aware that value creation is a sensitive topic, all the more that in Europe venture capital has not proven a real correlation with value. It may even have destroyed more value than created any…

I had never mentioned here Federico Faggin, another European who became a serial entrepreneur in Silicon Valley. He was at EPFL today where he delivered an amazing speech about creativity and courage, the two elements inventors, innovators and entrepreneurs critically need. If you do not know him, just rush to his wikipedia page: “an Italian physicist, inventor and entrepreneur, widely known for designing the first commercial microprocessor. […] He was co-founder, with Ralph Ungermann, and CEO of Zilog, the first company solely dedicated to microprocessors. He was also co-founder and CEO of Cygnet Technologies and of Synaptics.”

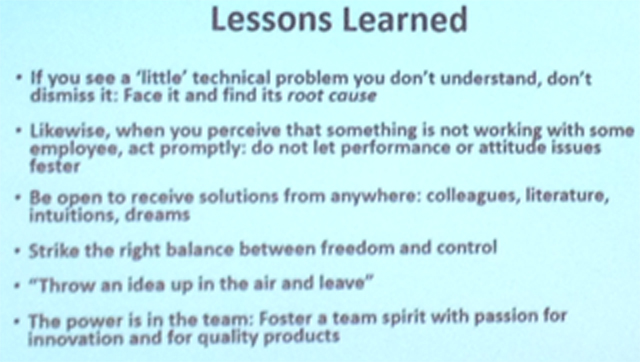

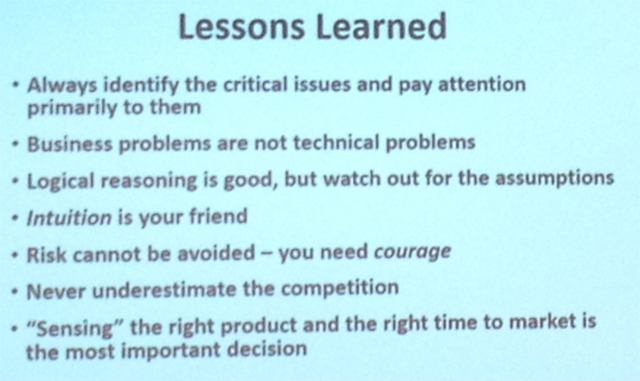

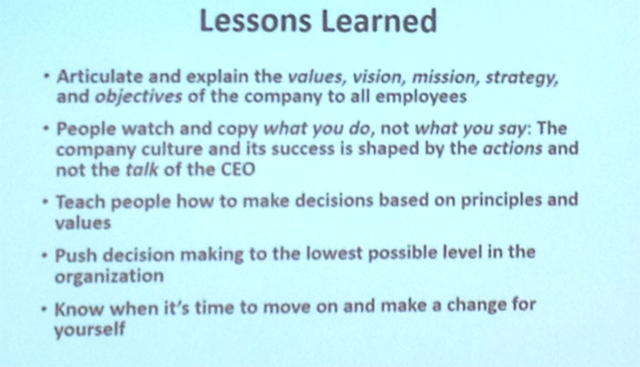

I hope his talk will be put online, in which case I will give the reference later. In the mean time, here are just 3 pictures (taken by a colleague, thanks!) about his lessons learned.

– If you see a ‘little’ technical problem you don’t understand, don’t dismiss it: Face it and find its root cause

– Likewise, when you perceive that something is not working with an employee, act promptly: do not let performance or attitude issues fester

– Be open to receive solutions from anywhere: colleagues, literature, intuitions, dreams

– Strike the right balance between freedom and control

– ‘Throw an idea up in the air and leave’

– The power is in in the team: Foster a team spirit with passion for innovation and for quality products

– Always identify the critical issues and pay attention primarily to them

– Business problems are not technical problems

– Logical reasoning is good but watch out for the assumptions

– Intuition is your friend

– Risk cannot be avoided – you need courage

– Never underestimate the competition

– ‘Sensing’ the right product and the right time to market is the most important decision

– Articulate and explain the values, vision, mission, strategy and objectives of the company to all employees

– People watch and copy what you do, not what you say: The company culture is shaped by the actions and not the talk of the CEO

– Teach people how to make decisions based on principles and values

– Push decision making to the lowest possible level in the organization

– Know when it’s time to move on and make a change for yourself

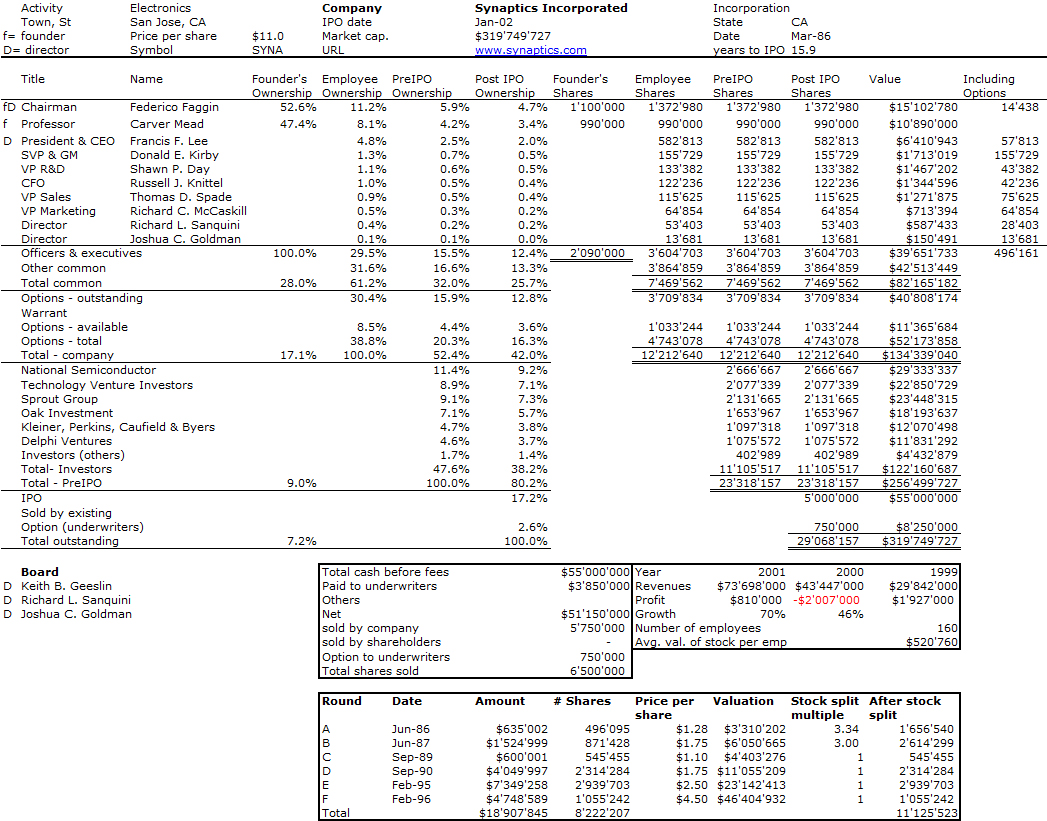

As a conclusion to this post, here is my usual cap. table when I have data about founders. Here is Synaptics.

After my initial notes (part I), the importance of culture (part II), the recipe (

The subtitle of the chapter is “Big V, Little C” and their quote to begin the chapter is “if you want to make money, do private equity. If you want to have fun, do venture capital”. They then borrow to AnnaLee Saxenian: “In Boston it was the entrepreneurs who dressed nicely and showed up on time to impress the investors. In Silicon Valley it was the opposite.” […] “In other words, the venture – that is the startup – is always more important than the capital, with a Big V and a Little C.” [Pages 218-21]

They explain why investing in the seed and early stage is costly for venture capitalists. “It’s better to buy a wonderful company at a fair price than a fair company at a wonderful price. […] Investing earlier in a deal must be counter-balanced by a strong potential of a massively disproportionate payout at the end. Otherwise, it is simply not worth the risk. […] Lowered transaction costs due to trust and social norms make high-risk seed-stage and early-stage venture capital more profitable [in Silicon Valley].” [Pages 228-29]

In other areas, subsidized capital plays a role. But it does not mean VC should not be understood: “There are two ways to build a venture fund. One takes as little as thirty minutes to learn. The other can take twenty years or more. The short course is to learn the formal legal structuring and financial processes of a typical venture fund. […] the more difficult and time-consuming course is to learn the human behavioral dynamics that happen in and around venture funds. […] Questions such as:

– how do you treat others in situations where mistakes and failures happen almost daily?

– how to build a reputation for trust, candor and integrity when millions of dollars are at stake?

– what type of value can you provide an entrepreneur who probably knows far more about the business than you do?

– how do you actively listen to an entrepreneur, and then see beyond their words to the true prospects of a company?

– how do you know when a CEO is not fit to run a company anymore?

– how do you help a tiny company build life-or-death relationships with huge, powerful customers or strategic partners?”

It reminds me what I learnt 20 years ago: it takes 5 years and $10M to make an investor.

The authors conclude their chapter with marvelous documentary SomethingVentured: “[VCs]’re working really hard, they’re very bright, they’re working together, and they’re collaborating. And there’s a lot of fun involved in achieving things together as a group. So I don’t think you can underestimate how much fun the people… had doing what they did. I think they’re extremely proud, but when they talk about these stories, they’re laughing, they’re smiling. There’s just this excitement and energy about building something.” [Page 242]