Another must read about the crisis of our times. Following Piketty or others, or lesser known analysis of Small-Town America of living anywhere vs. somewhere, here is J. D. Vance’s “great insight into Trump and Brexit”.

If ethnicity is one side of the coin, then geography is the other. [Page 3]

It is unsurprising, then, that we’re a pessimistic bunch. What is more surprising is that, as surveys have found, working-class whites are the most pessimistic group in America. More pessimistic than Latino immigrants, many of whom suffer unthinkable poverty. More pessimistic than black Americans, whose material prospects continue to lag behind those of whites. While reality permits some degree of cynicism, that fact that hillbillies like me are more down about the future than many other groups – some of whom are clearly mode destitute than we are – suggests that something else is going on. [Page 4]

The scale of migration was staggering. In the 1950s, thirteen of every one hundred Kentucky residents migrated out of state. Some areas saw even greater migration: Harlan county, for example, which was brought to fame in an Academy Award-winning documentary about coal strikes, lost 30 percent of its population to migration. In 1960, of Ohios’s ten million residents, one million were born in Kentucky, West Virginia, or Tennessee. This doesn’t count the large number of migrants from elsewhere in the southern Appalachian Mountains; nor does it include the children or grandchildren of migrants who were hill people to the core. [Page 28]

Mamaw’s family participated in the migratory flow with gusto. Of her seven siblings, Pet, Paul, and Gary moved to Indiana and worked in construction. Each owned a successful business and earned considerable we lath in the process. Rose, Betty, Teaberry, and David stayed behind. All of them struggled financially, though everyone but David managed a life of relative comfort by the standards of their community. [Page 29]

A Mind at Play is a very interesting book for many reasons. The subtitle “How Claude Shannon Invented the Information Age” is one reason. It is a great biography of a mathematician whose life and production are not that well-known. And what is Information? I invite you to read these 281 pages or if you are too lazy or busy, at least the Shannon page on Wikipedia.

What I prefer to focus on here is the ever going tension between mathematics and engineering, between (what people sometimes like to oppose) pure and applied mathematics. Pure mathematics would be honorable, applied mathematics would not be, if we admit there is such a thing as pure or applied maths. So let me extract some enlighting short passages.

The typical mathematician is not the sort of man to carry on an industrial project. He is a dreamer, not much interested in things or the dollars they can be sold for. He is a perfectionist, unwilling to compromise; idealizes to the point of impracticality; is so concerned with the broad horizon that he cannot keep his eye on the ball. [Page 69]

In Chapter 18, entitled, Mathematical Intentions, Honorable and Otherwise, the authors dig deeper: Above all [the mathematician] professes loyalty to the “austere and often abtruse” world of pure mathematics. If applied mathematics concerns itself with concrete questions, pure mathematics exists for its own sake. Its cardinal questions are not “How do we encrypt a telephone conversation?” but rather “Are there infinitely many twin primes?” or “Does every true mathematical statement have a proof?” The divorce between the two schools has ancient origins. Historian Carl Boyer traces it to Plato, who regarded mere computation as suitable for a merchant or a general, who “must learn the art of numbers or he will not know how to array his troops.” But the philosopher must study higher mathematics, “because he has to arise out of the sea of change and lay hold of true being.” Euclid, the father of geometry, was a touch snobbier “There is a tale told of him that when one of his students asked of what use was the study of geometry, Euclid asked his slave to gibe the student threepence, ‘since he must make gain of what he learns’.”

Closer to our times, the twentieth-century mathematician G. H. Hardy would write what became the ur-text of pure math. A Mathematicians’ Apology is a “manifesto for mathematics itself,” which pointedly borrowed its title from Socrates’ argument in the face of capital charges. For Hardy, mathematical elegance was an end in itself. “beauty is the first test,” he insisted. “There is no permanent place in the world for ugly mathematics.” A mathematician, then, is not a mere solver of practical problems. He, “like a painter or a poet, is a maker of patterns. If his patterns are more permanent than theirs, it is because they are made with ideas.” By contrast, run-of-the-mill applied mathenatics was “dull,” “ugly”. “trivial” and “elementary” And one (famous) reader of Shannon’s paper dismissed it with a sentence that would irritate Shannon’s supporters for years: “The discussion is suggestive throughout, rather than mathematical, and it is not always clear that the author’s mathematical intentions are honorable.” [Pages 171-2]

This reminds me of another great book I read last year Mathematics without apologies with one chapter entitled “Not Merely Good, True and Beautiful”. Shannon was a tinkerer, a term I discovered when I read Noyce‘s biography, another brilliant tinkerer. He was a brilliant tinkerer and he was a brilliant mathematician. He had himself strong vues about the quality of scientific research (pure or applied – who cares really?): we must keep our own house in first class order. The subject of information theory has certainly been sold, if not oversold. We should now turn our attention to the business of research and development at the highest scientific plane we can maintain. Research rather than exposition is the keynote, and our critical thresholds should be raised. Authors should submit only their best efforts, and these only after careful criticism by themselves and their colleagues. A few first rate research papers are preferable to a large number that are poorly conceived or half-finished. The latter are no credit to their writers and a waste of time to their reader. [Page 191]

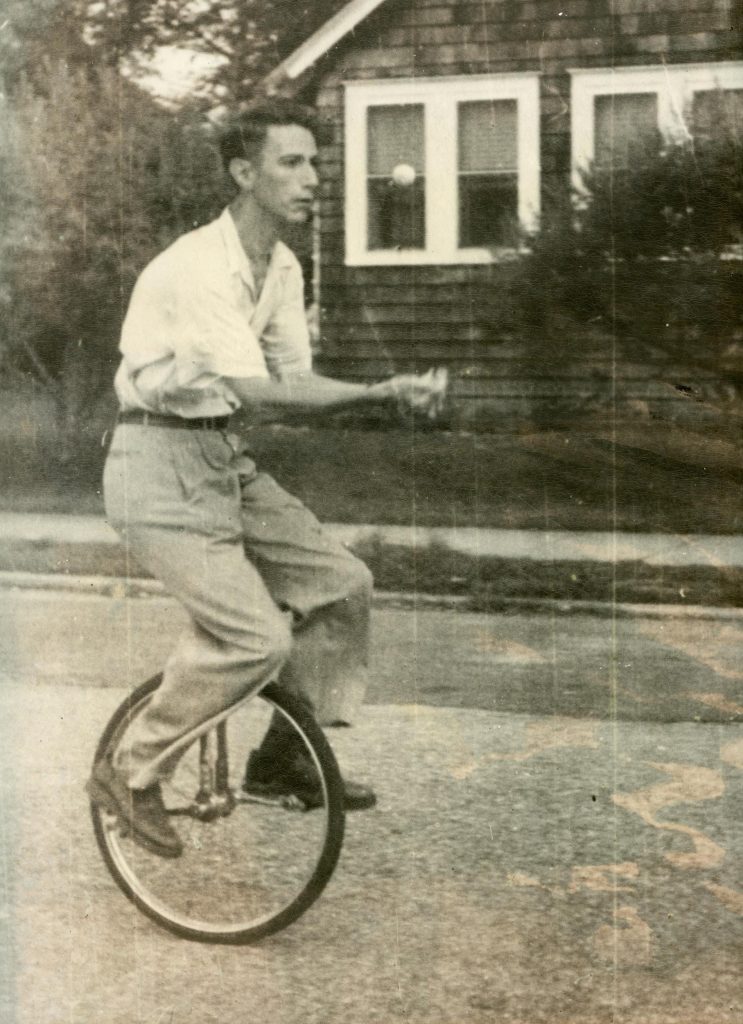

A brilliant tinkerer as the video below shows…

and it seems he designed and built the (or one of the) first computer that played chess. He was a juggler and a unicycler.

In the chapter Constructive Dissatisfaction, the topic is intelligence. It requires talent and training, but also curiosity and even dissatisfaction: not the depressive kind of dissatisfaction (of which , he did not say, he had experienced his fair share), but rather a “constructive dissatisfaction”, or “a slight irritation when things don’t look quite right.” It was a least, a refreshing unsentimental picture of genius: a genius is simply someone who is usefully irritated. He had also proposed six strategies to solving problems: simplifying, encircling, restating, analyzing, inverting and stretching. You will need to read that section pages 217-20.

He was also a good investor. In fact he was close to a few founders of startups and had a privileged access to people like Bill Harrison (Harrison Laboratories) and Henry Singleton (Teledyne) and although he used his knowledge to analyze stock markets. Here is what he has to say about investing: A lot of people look at the stock price, when they should be looking at the basics company and its earnings. There are many problems concerned with the prediction of stochastic processes, for example the earnings of companies… My general feeling is that it is easier to choose companies which are going to succeed, than to predict short term variations, things which last only weeks or months, which they worry about on Wall Street Week. There is a lot more randomness there and things happen which you cannot predict, which cause people to sell or buy a lot of stock. To the point of answering to the question of the best information theory for investment with “inside information.” [Page 241-2]

I could have tweeted only (and not blogged) about the picture below. Its author whom I met today authorized me to put it online. It is good to remember the fundamentals, the basics of entrepreneurship. It does not mean entrepreneurs do not need support, but not too much except if they are too fragile. In the past I had heard many similar things (incubators – incinerators?), and Wikipedia explains that incubators have various functions such as a device used to care for premature babies in a neonatal intensive-care unit, a device for maintaining the eggs of birds or reptiles to allow them to hatch. Once they are out of incubators, at least they are ready for accelerators…

“Incubators are for Chickens – In Doers We Trust.”

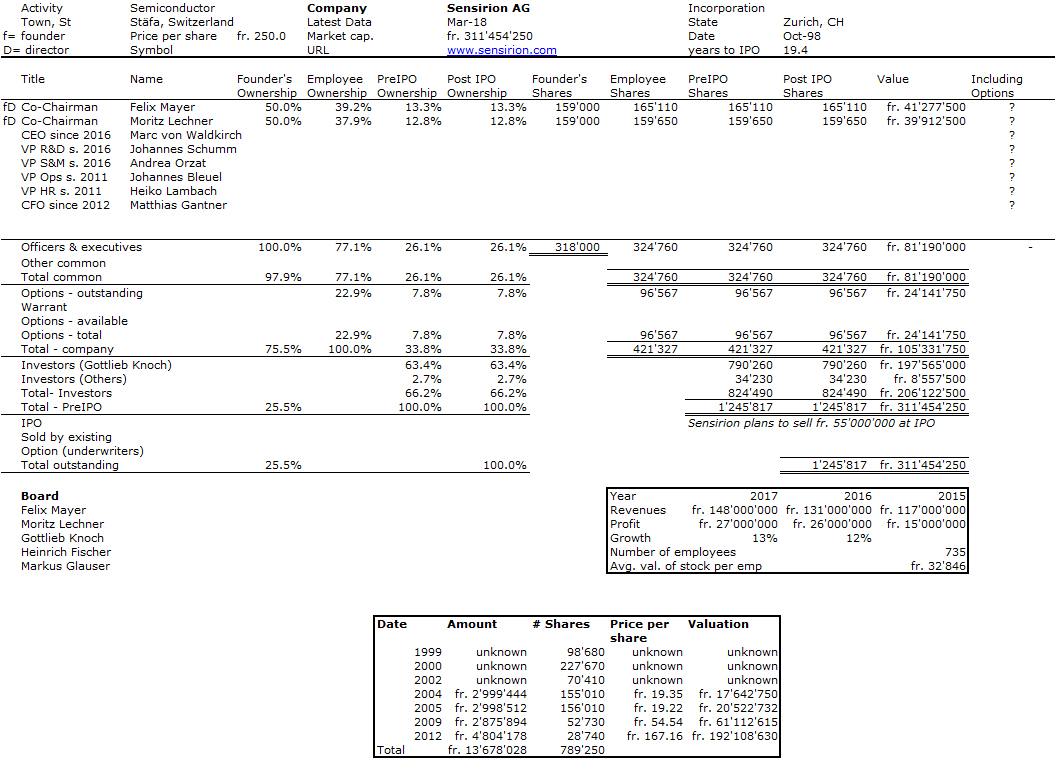

Sensirion finally announces its IPO. The spin-off from ETH Zurich was founded in 1998 and many were expecting such an event from a very succesful but quite discrete company. Sensirion has disclosed some numbers and I had followed the development of the company thanks to some data from the Zurich register of commerce. So as usual here is my guess of the capitalization table. And I look forward to compare it with the data from the IPO prospectus when it will be published…

Felix Mayer and Moritz Lechner, co-founders of Sensirion

Again this is guessing only. As you might see, the early funding rounds are unknown to me. I am not sure about how many shares the founders, main investor and employees have adn I am not sure either at which price the company will be priced. I based my numbers on about twice the company sales in 2017… The company claims Knoch has 55% of the company, the founders 14% and employees 8.5%. It does not look to far…

The Sensirion IPO prospectus is not public and is confidential so I cannot publish more than I have here. I can only write I was not too far from the truth despite some discrepancy…

About to give my optimization class this morning, I just remembered only one woman got the Fields Medal. This was in 2014. Unfortunately she died of cancer last year

Maryam Mirzakhani (3 May 1977 – 14 July 2017) became the first Iranian and first and only woman to win the Fields Medal.

Let me add, that in the field of optimization, apparently only one woman got the Dantzig Prize, Eva Tardos.

I have to admit, I did not take the time to think of a similar name for startups and innovation. Comments welcome…

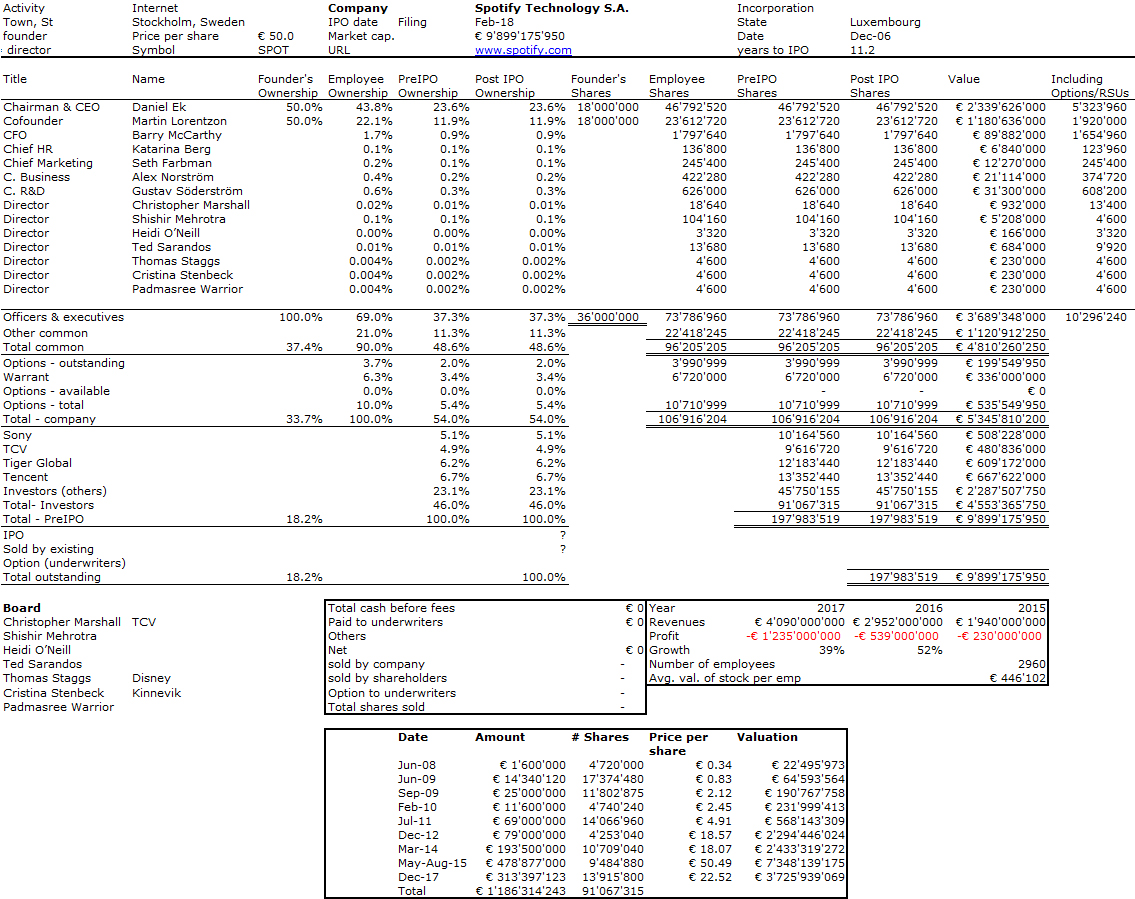

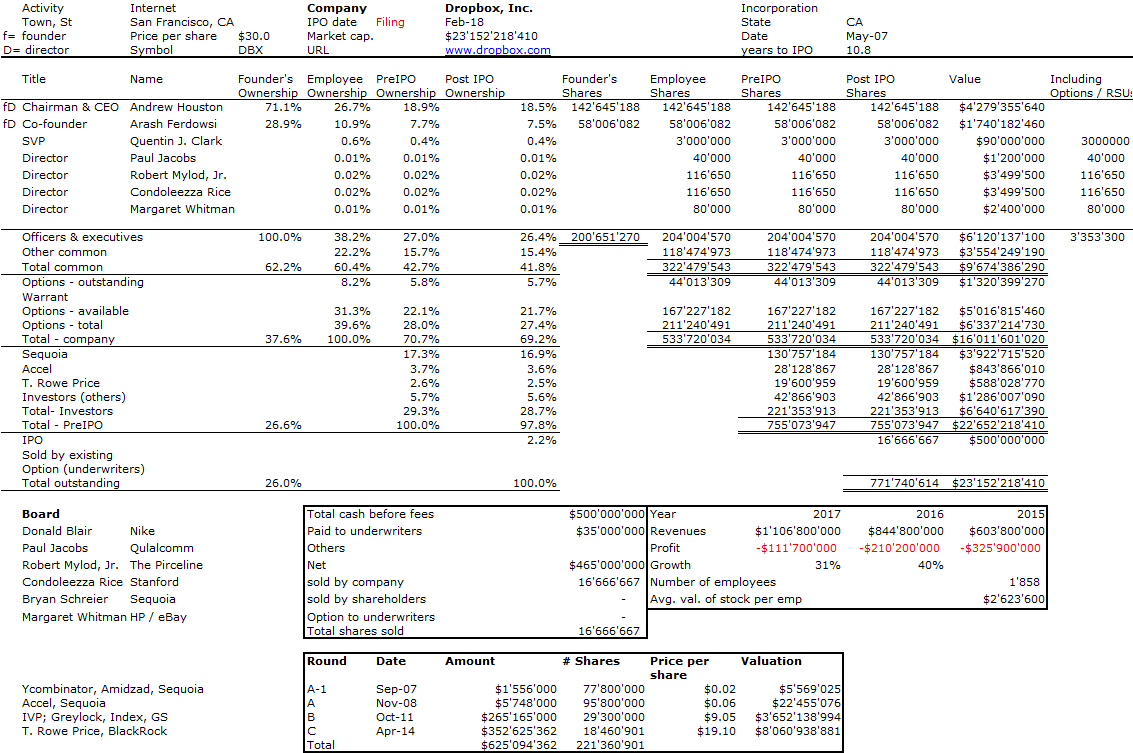

A few days after Dropbox filing for an IPO, here is Spotify. Their F-1 can be found here. The data from the filing document is not exhaustive enough for me, many pas financing rounds are not described but the Luxembourg register of commerce helps too.

Spotify founders Martin Lorentzon and Daniel Ek

Just like for Dropbox, this is a filing only, so the price per share is tentative and the valuation is not fixed yet. The price per share could probably go from €20 to €100…

I have never been a big fan of “How to” books, sometimes called “personal development”. Even if Reid Hoffman is a brilliant entrepreneur, he did not really change my mind with his Start-up of You. His book which sometimes look like an ad for LinkedIn and which is strangely written with four hands, one saying I (Reid) and the other, He (Ben Casnocha) is still a good description of what it requires to look at improving a career:

– know thyself,

– be adaptable,

– network,

– look for opportunities,

– assess risks.

He also has beautiful ideas. When he quotes authors such as Jonathan Franzen – “Inauthentic people are obsessed with authenticity” – or David Foster Wallace – “There is no experience you have had you are not the absolute center of”. (Pages 93-94) I assume Hoffman knows Franzen and Wallace were great friends until the death of the second – strong ties in networks.

He also prones diversity in networks. If people know each other too well, there is not enough diversity, if they do not each other well enough however, trust is tougher to build. You need both old blood (trust) and fresh blood in a team. (Page 118)

But a team is only as good as its members. team quality requires individual quality. Look below at the famous Paypal mafia(Page 159)

Even if Hoffman gives good advice t the end of each chapter, he is not over-analyzing. For example, when talking about risks: Of the voluminous research on risk, remarkably little of it actually analyzes how real businesspeople make real decisions in the real world. An exception is a study done by professor Zur Shapira in 1991. (…) What he found likely came as a disappointment to architects of fancy decision trees. The executives surveyed didn’t calculate the mathematical expected value of various scenarios. They didn’t draft long lists of pros and cons. Instead, most simply tried to get a handle on a single yes-or-no question: could they tolerate the outcome if the worst-case scenario happened?

Impressive panel @ESPCI_Paris #SiliconValleyinParis with @reidhoffman @tfadell @Hemaisphere, Sebastian Amigorean and Stephen Quake moderated by @APapiernik

You could ask me why I decided to read that book. In the end, it shows entrepreneurs are really good at action, less at analysis… The truth is I went to Paris to listen to him at a great event called Silicon Valley comes to Paris. I wanted to approach him, network! Without knowing I applied some his advice and also made some of the mistakes he is describing. My main mistake was not knowing his interest about European start-ups. In fact he has not invested in Europe, he does not know EPFL. It makes you humble and willing to network even further. Reid, would you come back in Europe and inspire aspiring young entrepreneurs?

While Trump and Harari were in Davos, I visited Silicon Valley for the nth time. Even more than during my last trips in 2014 and 2016, I could feel the gap that has been created between the Silicon Valley that I discovered and loved in the late 80s and the one that exists today (and that I still love).

As one of my interlocutors mentioned, the Hippie generation – which Leslie Berlin describes in her Troublemakers and which until Brin and Page tried to democratize technology – has been replaced by the Libertarian self-interest of social networking that even Reid Hoffman will have a hard time to balance (see It’s time to change the culture of Silicon Valley). The skyscrapers climb in San Francisco, the poor had to leave or live in tents all over the bay, the venture capital funds do not perform as one might think, the unicorns might disappear one after the other, it takes 3 hours to drive from Berkeley to Palo Alto at 6am, one finds more founders than entrepreneurs according to Leslie Hook, and even Steve Blank is looking at a little less at startups and focuses more on innovation of government organizations.

This is a bit the “Querelle des Anciens et Modernes” and I am not sure Steve Jobs would pass the baton to this new generation when he said in 2005[death] clears out the old to make way for the new. Some think that Silicon Valley is reaching its limits, but AnnaLee Saxenian said the same thing … in 1979. Will we live old enough to have the answer?

I had read a few years ago the great The Man Behind the Microchip by Leslie Berlin. After the biography of Robert Noyce, one of Intel’s cofounders, Berlin comes now with Troublemakers, a description of “How Generation of Silicon Valley Upstarts Invented the Future”.

The title is a reference to a famous Apple advertisement: The crazy ones. The misfits. The rebels. The troublemakers. One of the great merits of the book is to focus on 7 individuals (2 women and 5 men) which are relatively unknown compared to the stars of Silicon Valley. Will you recognize them on the following image? (The answer is at the end of the post).

The book is not only great storytelling. It describes the dynamics of Silicon Valley from the late 60s to the early 80s and how “five major industries — personal computing, video games, biotechnology, modern venture capital, and advanced semiconductor logic — were born”. You can also listen to Leslie Berlin here:

The close-to-400 page book also has more than 80 pages of rich notes. It is really a must read for anyone passionate or just interested in Silicon Valley. Here are a few quotes:

Indiana Jones: I’m going after that truck.

Sallah: How?

Indiana Jones: I don’t know. I’m making this up as I go.

“We didn’t want to be considered part of the flock. Eagles don’t flock, was our joke.” (Tom Perkins when asked why KP was not initially on Sand Hill Road – Page 192)

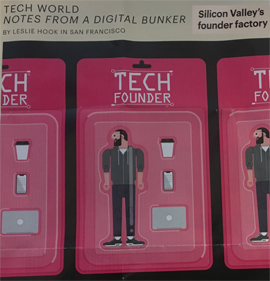

Let me make a short parenthesis. While reading this book, I read a very interesting article in the FT entitled Silicon Valley’s founder factory ‘Silicon Valley is lacking in one core area — a sense of entrepreneurial hustle’ (Leslie Hook – Jan 2018): “When I moved to San Francisco four years ago, I noticed something odd about the start-up founders I met: many of them resembled each other. Not just physically, though most were men under 35. But also in the way they spoke about their companies. They had PowerPoints at the ready, and big numbers on the tips of their tongues. Everyone seemed to know exactly what the total addressable market of their start-up was, even if they hadn’t yet made a single dollar of sales. […] By contrast, while there are a lot of founders in Silicon Valley, I have found relatively few entrepreneurs. The founders are smart and hard-working. But many are simply products of a system, which is why they all seem vaguely the same.” Interesting food for thought in comparison to the 70s…

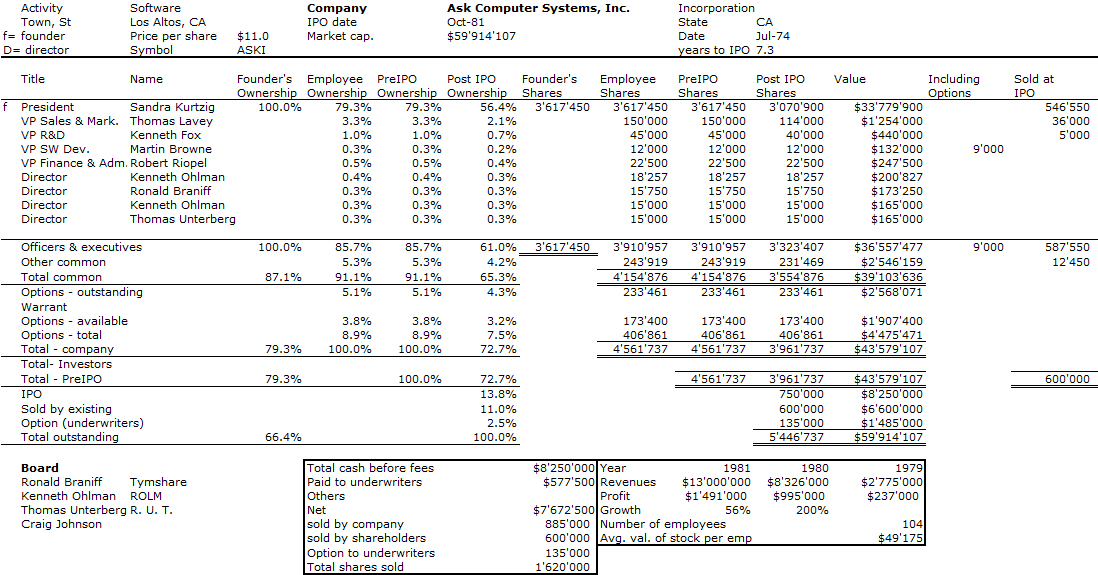

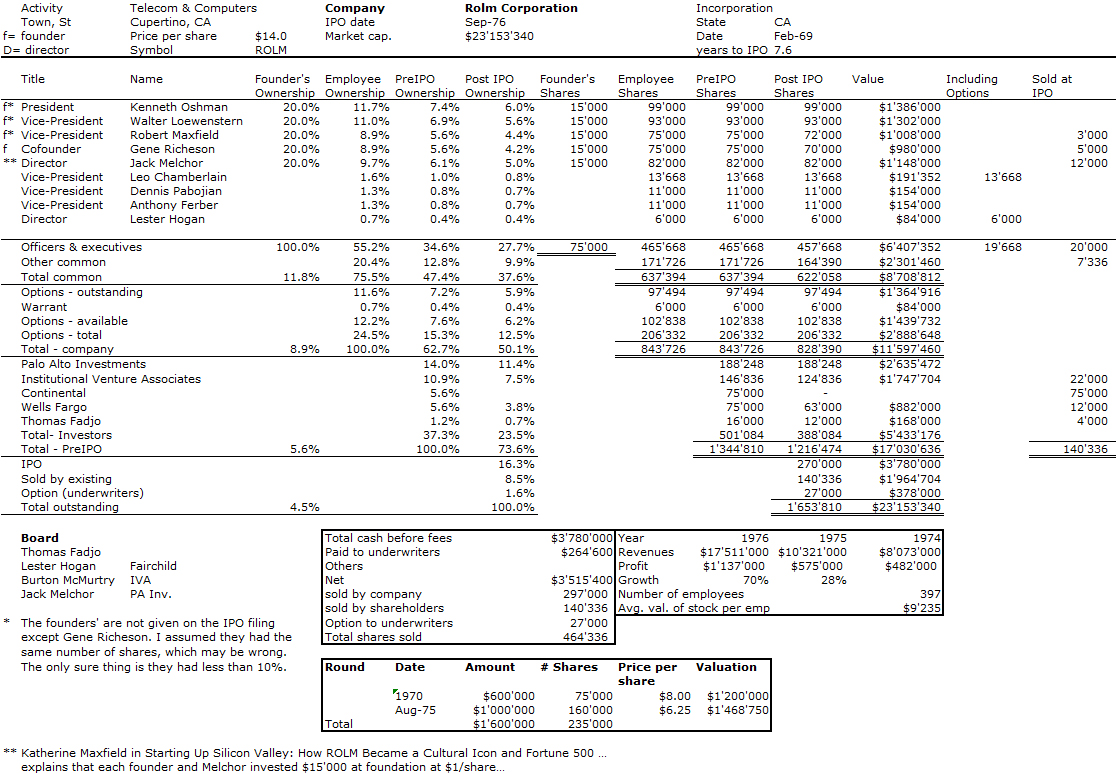

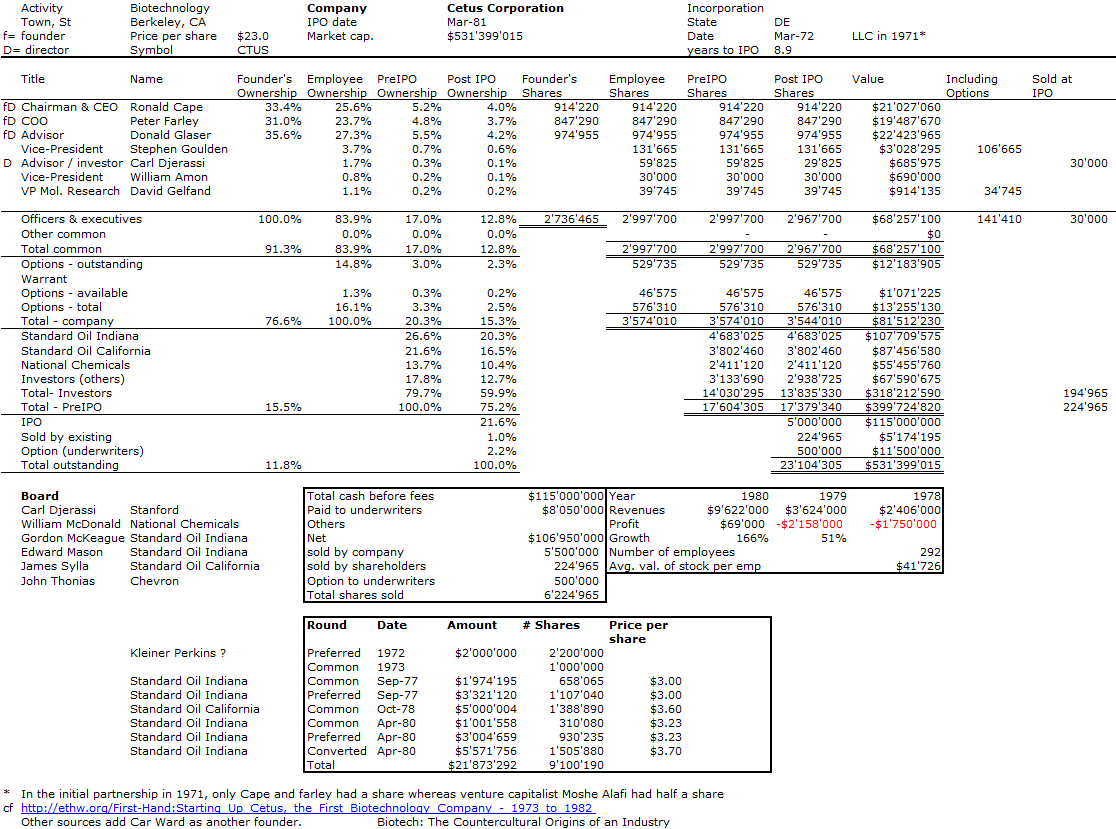

As my personal contribution, here are 4 of my “usual” cap. tables. Ask Computer, ROLM, Cetus and Atari are companies from the 70s mentioned in the book that I had not studied yet… Ask was one of the first software companies and Cetus the 1st biotech company…

Ask Computer cap. table

ROLM cap. table

Cetus cap. table

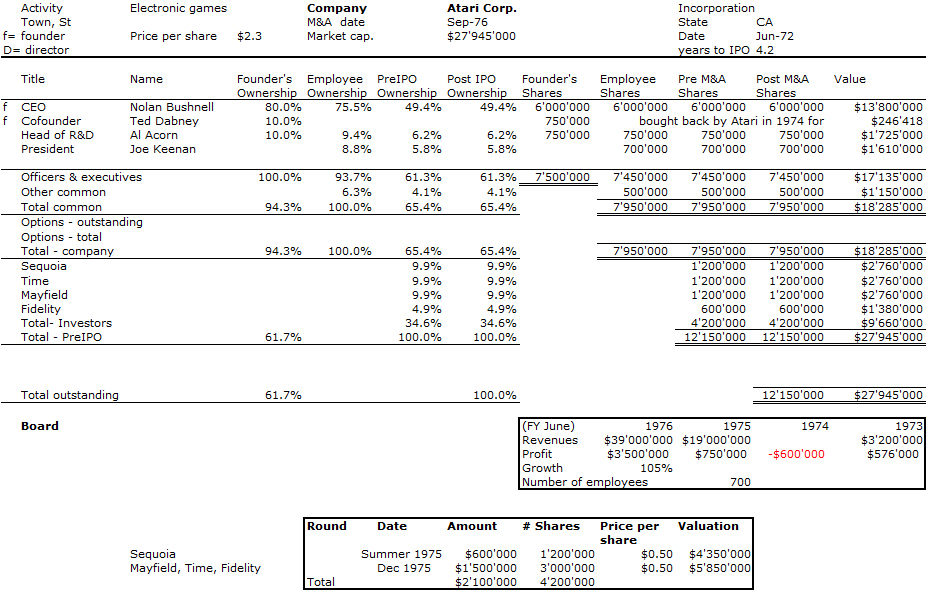

Atari cap. table

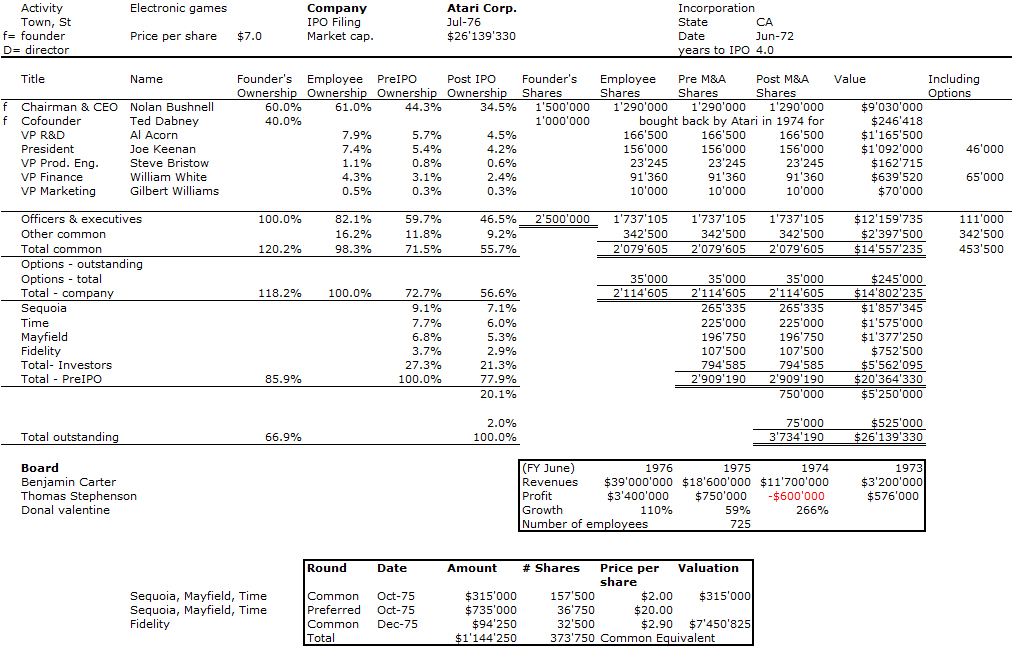

Well to show the complexity of the exercise, here is a second Atati cap. table based on its S-1 IPO Filing…

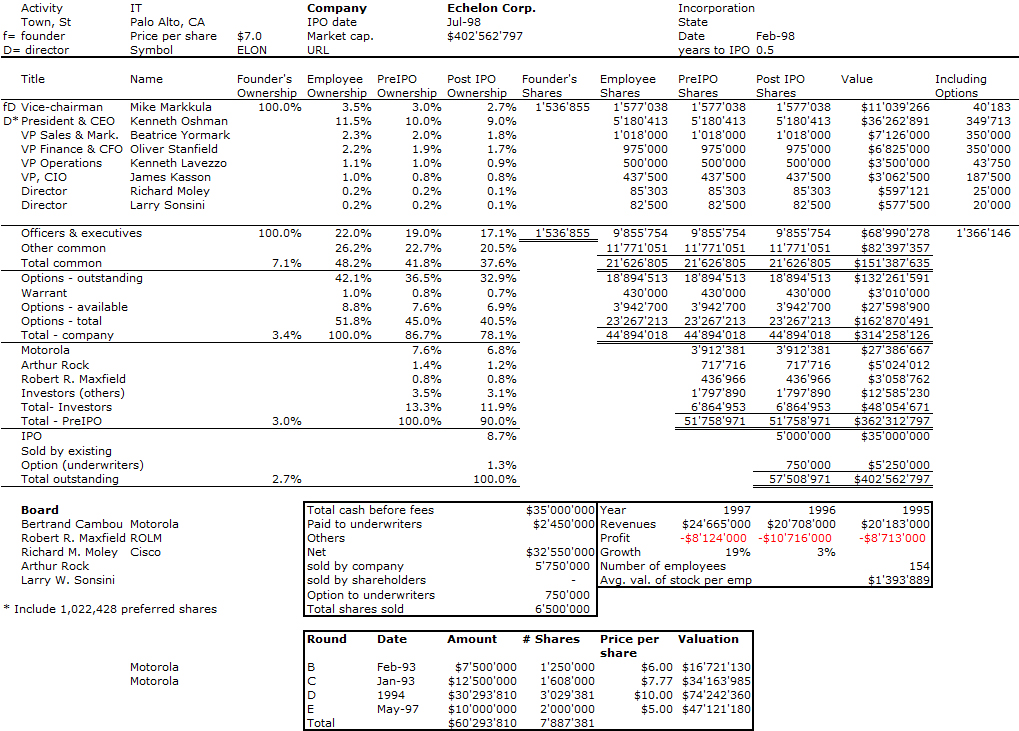

In her final pages, Leslie Berlin also mentions another company founded by Mike Markkula, Echelon Corp. Echelon had the ROLM founders as well as Arthur Rock and Larry Sonsini as stakeholders. Here is a 5th table: